Visa and Mastercard’s Q3 financial results are well covered elsewhere. At Business of Payments, we’re more interested in what the investor updates tell us about trends in the European market and the success (or otherwise) of new products.

Mastercard continues to outperform Visa in Europe although its pace of growth has moderated. The two schemes are now almost neck and neck. Mastercard’s merchant payment volume grew 26% in Q3 to $602m while Visa’s was up 20% to $637m. Total scheme volume was up 23% in dollar terms although this falls to 14% when calculated in euros. Overall ATV was steady at $36.24.

European politicians and regulators have long been worried about an over-reliance on US payment networks. The European Payments Initiative and the Digital Euro are two of the latest responses. Asked about the threat of protectionism, MichaelMiebach, Mastercard’s CEO was adamant that his business would always have a role in any payment ecosystem saying. “We’re seen as a technology company, a global technology company, not necessarily as a US payment brand.” That’s a bold statement and one which does not align with current sentiment at the European Central Bank and elsewhere. Dependence on foreign owned payment systems is a risk for any jurisdiction.

Last week, Worldline’s profits warning highlighted weakening European payment volumes, especially in Germany but Miebach said he saw no slowdown. “Consumer spending remains pretty steady in Germany and generally in Europe…. So Europe’s been a bright star, continues to be for us. So we don’t quite relate to what others are reporting.”

Portfolio wins

The deceleration in Mastercard’s European volume growth is primarily due to the removal of the NatWest portfolio win (16m cards) from the annual comparisons. But Mastercard has continued to win new card portfolios including 10m Deutsche Bank cards and 20m from UniCredit. Miebach said the Deutsch Bank conversion “has already started. It’s a combination of debit and credit. It will happen over an extended period of time. It’s not a flip-the-switch kind of scenario.”

Mastercard is also working with issuers to migrate more than 100m Maestro cards (mainly in Germany and the Netherlands) to its own-brand debit product. This is good news for consumers as their cards will now work online. It’s less good news for merchants who will be faced with higher transaction charges.

Visa is also positive about Europe, remarking that it has opened seven new locations over the last five years and more than doubled its workforce. Visa claims more than 100 relationships with European fintechs and even bought two of them – Tink (open banking) and CurrencyCloud (cross-border money transfers).

Excluding Maestro, the total number of Mastercards in Europe rose 13% increase to 796m. Visa did not publish numbers for card this quarter but reported that, excluding the UK, the number of active Visa cards in Europe is up 50% since 2019. Including the UK, where it has lost one third of the debit market to Mastercard, the figures would not seem so pretty. However, Visa’s management says it expects to migrate 40m cards from 40 issuing clients in Europe over next few years. The company says that these incomings portfolios are skewed to high margin cross-border transactions.

Tokenised transactions

Increasingly, cards are tokenised which means that the fraud-prone 16 digit PAN is not included in the transaction data. Visa processed 14bn tokenised transactions worldwide in Q3, up 60% year on year. Tokens make card transactions significantly more secure, and this means that issuers are much less likely to block them. This is very good news for merchants. Ryan McInerney, Visa’s CEO, said “we’re seeing, on average, somewhere between 4% and 5% higher approval rates across our partners. And we also see it with a reduction in fraud — a 30% reduction in fraud.”

Mastercard reported “the number of tokenized transactions has more than doubled over the past two years. We just processed over three billion tokenized transactions in one month.” Management highlighted the importance of tokens in allowing Mercedes-Benz customers in Germany to “pay for fuel directly from their vehicle using only their fingerprint.”

Open banking

Although Visa was blocked from buying Plaid, an open banking leader in the US, it was able to acquire Tink, a similar business HQ’d in Sweden. Management said that Tink “continues to perform very well in Europe…and we look forward to the opportunity to bring Tink outside of Europe.”

Mastercard has acquired Token, another European open banking provider. Questioned about the commercial model for the schemes to enter open banking, Mastercard’s Miebach said “We’re putting in our open banking connection to make it clear is there a balance on the account. It’s called the payment success indicator. That is the product. And it is a per-click fee related to the API call. So that is the model.”

Contactless

Mastercard says contactless now represents 63% of face-to-face transactions globally. Miebach explained why mass transit was so important. “By converting transit to Open-Loop, we gain access to more low-ticket, high-frequency transactions, both at the station and the surrounding merchants.”

Visa reports 76% of all F2F transactions outside the US are contactless, up 5ppts. The US is growing more quickly, albeit from a lower base. Contactless share was up 13ppts to 40%. Rapid transit is driving adoption worldwide. Visa says it enabled 150 new transit systems for contactless, taking the global total to 750. Impressively, 40% of these new customers are using Cybersource, Visa’s in-house acceptance solution, as their payment gateway.

Gateways

Cybersource seems to be out-performing Mastercard Gateway Services, its direct competitor. Cybersource attracted 2,600 additional customers in 100 countries in Q3. McInerney put its success down to investments in omni-channel, tokenisation (vital for mass transit) and fraud prevention capabilities.

Both schemes have products that allow money to be sent to one of their cards. Visa reported 7.5bn Visa Direct transactions globally in Q3 up 19%. In Europe, it is supported by 1000 programmes managed by 100 Visa partners. McInerney said Visa Direct is “focused on bill payments, on earned wage access, on insurance disbursements, on P2P more broadly in new geographies around the world, both domestic and cross-border.”

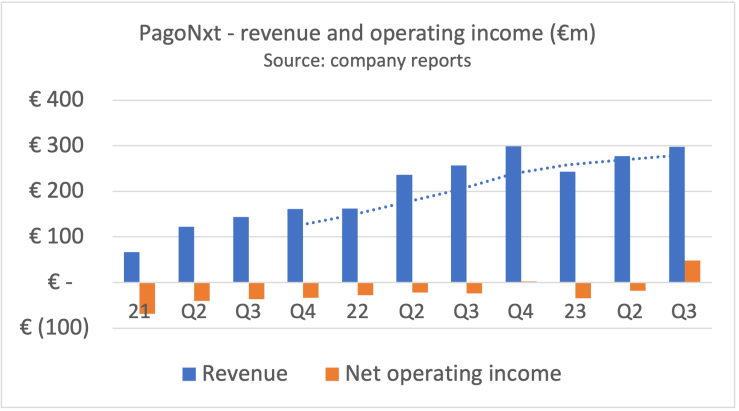

Lifting the gloom a little, PagoNxt, Santander’s payment business, reported sparkling Q3 results including a maiden operating profit. This performance highlights the success of Santander’s decision to in-source and consolidate its payment activities. PagoNxt comprises all of Santander’s payment assets, including Getnet, a leading multi-national merchant acquirer, trade finance expert Ebury, Payments Hub which brings together the bank’s account to account transactions, and Superdigital, a financial marketplace for the economic inclusion of the underbanked.

Q3 merchant payment volume was up 27% to €54bn “backed by good merchant performance” in Mexico, Brazil, and Europe and share gains in all core markets. Transactions grew 26%, leaving ATV steady at €22.46.

Management gave few other updates but said that the Payments Hub is “already one of the largest processors of A2A” in Europe and is now processing transactions from Santander businesses in Spain and the UK.

Overall revenue was up 16% in Q3 to €298m but expenses fell 11% to €251m. It’s not clear what has led to the decline in operating costs but the impact on operating profits was very positive. PagoNxt reported an operating profit of €48m for the quarter at a healthy 16% operating margin, compared with a loss of €24m in 2022. It will be interesting to see whether this is a blip or the first step towards steady growth in profitability.

Barclays has updated investors on its strategic review of Barclaycard, the UK’s leading card issuer and the second largest merchant acquirer. Reuters reported in August that Barclays had hired consultants to advise “whether some of the payments businesses should be expanded or combined with other providers through a merger or joint venture.”

Confirming for the first time that a review of merchant acquiring was underway, C.S. Venkatakrishnan, Group CEO said “I think there’s a broader strategic question for us, which other banks have faced. [Payments is] a very technology-driven business. Is there a comparative advantage in developing the technology or in implementing the technology or is there a comparative advantage in helping service [merchants] as part of a larger set of banking services? That’s the question we’re looking at, and then I think the commercial arrangement will come out of the answer to that question. So, that’s the way we are thinking about that business.”

Despite its strong distribution through the bank’s network of business advisors, Barclaycard is believed to be losing market share in SME to Dojo and with larger corporates to Adyen and others. Lack of investment in new products is understood to be a the heart of the problem and could be addressed if the sales team had access to technology from a modern payment vendor.

If Barclays decides to divest its merchant acquiring business, several private equity funds, including Bain/Advent, would certainly be interested. A sale price of £2bn has been suggested based on EBITDA of £300m but management may struggle to achieve this following the sharp declines in the stock price of listed European payment businesses such as Adyen and Worldline. This might tip the balance towards incorporating Barclaycard inside a JV with a technology partner such as Fiserv, Nexi or Worldline. Two other major European banks are currently in processes to do just this – Sabadell with Nexi and Credit Agricole with Worldline.

Meanwhile Barclaycard UK acquiring volume recovered a little in Q3 to record 9% year on year growth, having increased just 4% in the previous quarter.

Following Adyen’s catastrophic H1 results, Worldline was next to shock the financial markets. Shares in the French processing giant fell 50% as management warned of lower profits due to “economic slowdown in some of our core countries,” notably Germany. Worldline also said it would terminate some German merchants generating €130m annual revenue. This move is believed to be linked to the German gambling regulator’s decision to clamp down on EU gamers which don’t have a local licence. In more bad news Bafin, the financial regulator, has restricted new customer onboarding at Payone, Worldine’s joint venture with German savings banks, citing money laundering and fraud concerns.

In a minor consolation for Worldine shareholders, the company bought the acquiring business of Banca del Fucina for €25m. The deal adds 5,500 POS generating €500m payment volume. The Rome-based bank will sell Worldline’s products through its 36 branches.

Nexi is another processor under pressure. The Italian group’s stock price has sunk 30% since its IPO in 2019 despite reporting good progress on integrating acquisitions of Nets (Nordics) and Concardis (Germany). Private equity groups, including CVC, are rumoured to be preparing bids although the Italian government still has a veto on any sale.

The relative underperformance of payment processors reflects concerns that payment acceptance is becoming commoditised. Checkout.com disagrees. In a new report, the London based processor says acceptance is becoming more complexand that the additional complexity brings margin opportunity. Checkout highlights the rise in cross-border payments, additional friction generated by strong customer authentication (SCA) and disjointed application of network tokenisation by issuers as factors running in its favour. You can read the full report here or a good summary by Enemigo.

Bucking the trend Boku, a London-listed processor, reported revenue up 26% in H1 2023as it successfully manages the transformation from carrier billing to global APM provider. Boku has a stellar client list including Amazon and Facebook and says it is now competing successfully with Thunes, dLocal and PPRO.

In corporate news Shift4, a US processor with strong in-house vertical software products, finally got the regulatory green light to proceed with the $575m acquisition of Credorax Finaro, the Israeli HQ’d acquirer/processor. The enlarged group will have the strong capability on both sides of the Atlantic that Shift4 needs to support Starlink, its marquee customer.

Rock solid delivery is at the heart of payment processing. If you can’t guarantee this, you won’t get a hearing for those wonderful value added services the product team has invented. Square went down for over 24 hours worldwide due to a DNS issue caused by “an utter failure in system testing.” Shift4 saw a golden opportunity to poach Square customers.

Although the outage will make it harder for Square to sell to larger merchants, established enterprise acquirers can have similar issues. Worldine went down one recent Saturday, causing chaos in supermarkets across France.

BNP Paribas is launching a marketplace payments start up in H1 2024. Called Panto (oh yes it is), the new business will include acceptance, pay-outs and automated boarding and is aimed at BNP’s current customers. Panto will be built by 321founded who claim to have put together a beta version in just 6 months.

Mollie, the Dutch payment unicorn which lost €121m in 2022, has announced further staff cutbacks. Following the departure of the CEO and CFO, 10% of employees will lose their jobs. Founder, Adrian Molle, “denied that the company board lacks vision and that there is a toxic work environment.”

New shopping

We’re keeping an eye on the development of autonomous stores as a possible accelerator of the switch in payment transaction from the POS to the shopper’s phone.

AiFi is a technology vendor with 100 stores operational worldwide including 50 Zabka Nano in Poland. AiFi solutions are also powering the Konzum Smart store, the first autonomous retail outlet in Croatia.

JUXTA, a US vendor, is commercialising portable autonomous stores which can be used at sports or music events. The company sees an opportunity to place them next to EV charging stations, so motorists can shop while waiting for their batteries to charge.

Some vendors are proposing facial recognition as an alternative to cards or Apple Pay. Payface, a Brazilian start-up which recently raised $2m, expects to have 2,000 stores live with its solution by the end of this year. The company just bought SmileGo, a competitor. But even facial recognition isn’t fool proof. Underaged delivery drivers in Brazil have been registering for work using photographs of their parents.

Primer’s product strategy makes sense. Orchestrators need to move beyond simply routing transactions if they want to generate significant revenues. Gr4vy, another orchestrator, has launched “vault as a service” in which it stores customers’ card details, billing and shipping details, linked to a vaulted card token. There’s no vendor lock-in which is very welcome. Merchants can export their data and move to another supplier.

Of course, anything “as a service” is only as good as the vendor supplying the product. Where the service is regulated, risk is heightened if the supplier’s processes are not up to scratch. UK based Modulr, a payment infrastructure provider that raised £83m in 2022, has been ordered by FCA to stop onboarding new customers. This is the latest intervention by European regulators. Railsr had its e-money licence revoked by Lithuanian authorities and Bafin, the German regulator, has restricted Solarisbank and PayOne from onboarding new customers.

One reason to upgrade to an Android terminal is for digital receipts. France outlawed the automatic issuance of paper receipts in August and the Belgian region of Wallonia has also banned retailers giving paper receipts unless shoppers specifically ask for one. There are no penalties for non-compliance, but the move gives the retail trade a welcome environmental nudge.

SoftPOS

Although Visa and Mastercard have pushed SoftPOS as a micro-merchant proposition to accelerate cash displacement, the business opportunity for the payment industry lies in enterprise. SoftPOS can revolutionise big company operations by bringing together multiple services on a single device and liberating staff from the till point.

Poland is fast developing into one of Europe’s leading SoftPOS markets. ING, which has 7,000 SoftPOS SME merchants has added Blik, the popular domestic mobile payment standard, as a payment option.

Polskie ePłatności, owned by Nexi and the second largest Polish acquirer, has launched PePpay a SoftPOS product in partnership with Danish start-up Softpay.io. Nexi has also announced SoftPOS in Italy to be distributed in conjunction with Banco Intesa Sanpaolo. There is no monthly fee and transactions under €10 are free of charge under the Government imposed micropayments initiative.

Elsewhere Tebi, a high profile Dutch start-up founded by Adyen alumni, is building its emerging payment business around SoftPOS. This is a fascinating move and offers the opportunity to see what happens when POS technology leaps a generation. Pricing is 5 cents per transaction + 2 cents for debit or interchange + 0.4% for credit.

Open banking

Many in the industry have been worried about the commercial viability of the emerging open banking sector. These concerns were underlined by 2022 financial results from Yapily and Truelayer, two well-funded start-ups. Truelayer, which claims market leadership in UK, Ireland, Spain and France and “significant share” in Germany and Netherlands, generated just £4m of sales in 2022. Together, Truelayer and Yapily lost £83m on combined turnover of just £7m. More details on the Business of Payments blog.

Very sensibly, Truelayer is using some of its cash for lobbying to help create a market for itself and has called on the EU to combine open banking with instant payments. This could create a domestic payment option for the EU that will “act as an alternative to the card duopoly” and create customers for open banking players.

Investors hoping for a quick turnaround in the industry’s fortunes will be heartened by Stripe’s announcement that it will be using Truelayer to offer open banking payments as an option for its merchants in 22 markets. The volume generated should be considerable, but Stripe will have driven a hard bargain and Truelayer may not see much margin.

Undeterred, Swedish open banking start-up Brite Payments has raised $60m to expand into 25 countries. Unlike many of its competitors Brite, which receives funds and settles with merchants, claims to be profitable already.

To succeed, open banking needs “scheme” rules, a well-publicised brand and an acceptance that all actors in the value chain will need paying. In the free enterprise model, where there is no profit, there will be no products.

The European Central Bank is making good progress with the Digital Euro and it’s hard to argue with the ECB’s statement that “The growing trend towards digital payments has also entailed increased European dependency on foreign service providers. A digital euro would also address risks stemming from geopolitical tensions. [COVID and Russian war] has painfully demonstrated the risks of relying exclusively on external suppliers for basic needs.”

The ECB is adamant that the digital euro is not “programmable money” and will safeguard “cash like levels of privacy”. There’s no rush. Central bankers now begin a two year “preparation phase” which involves finalising the rule book and selecting vendors for the platform and infrastructure.

Mastercard sense a business opportunity despite being one American vendors from which the ECB wants to reduce its dependence on. The network has launched its “CBDC Partner Programmefeaturing 7 vendors including Giesecke + Devrient, the German banknote printer.

In contrast, the digital dollar seems dead. It’s been killed by a combination of vested interests wanting to keep the current fabulously expensive US payment system going and conspiracy theorists convinced that digital currencies “undermine the American way of life.” Rich Turrin has a good summary of the evolving mess and Steve Forbes summarises the rather unhinged case against.

Crypto corner

We’re witnessing the prolonged death throes of the crypto bubble. Binance, the largest exchange, had its credit cards terminated by Visa and by Mastercard. Paradoxically, we’ve also learned that crypto/fiat volumes have been quite low. Visa has processed just $3bn from cards issued by 75 crypto exchanges since 2021. This makes sense: if you like crypto, why would you spend it?

Stable coins, which are pegged to traditional currencies, are said to offer the efficiency benefits of crypto but without having to worry about criminals and speculators. Yet Paypal’s stable coin dollars have not been wildly successful. Less than $10,000 daily volume is reported but it’s early days. Dave Birch says that PayPal’s stable coin might be the killer app for P2P cross-border payments. Others argue that there are now two kinds of PayPal dollars and that the stable coins, backed 1:1 by US Treasuries, are much the safer choice and will prove most popular.

The European Payment Initiative has chosen a brand. The new digital wallet facilitating account to account payment will be called “wero”, combining “we”, “euro” and “vero”. “The short and snappy sound resonates with the fast-paced nature of digital transactions,” said the CEO with a straight face. Wero will launch in Belgium, France and Germany by mid 2024 with the Netherlands next on this list.

Kristo Kaarmann, founder of Wise, discovered Singapore Airlines marking up an eDCC transaction by 5%. He wasn’t happy.

PCI-PAL, a London listed supplier of secure payment products for contact centres, won a resounding victory in its longstanding patent battle with US rival, Sycurio.

Fraudsters don’t always need crypto. Any Pilley, the colourful owner of CardSaver, a UK ISO, has been jailed for 13 years for mis-selling energy contracts to small businesses.

The metaverse didn’t last long. Banks are retreating from this short-lived hype cyclewith one vendor commenting “the urgency of these initiatives has been superseded by more pressing requirements.”

TrueLayer, the generously funded open banking unicorn, indicated just how costly its expansion plans have been. According to documents posted at UK Companies House, Truelayer Group reported group operating losses widening to £61m in 2022 on revenues of just £4m.

Founded by Franceso Simoneschi in 2016, TrueLayer is backed by a stellar rosta of investors including Stripe, Tiger Global and Anthemis. It has received funding of $272m in total (Crunchbase) with its $130m round in 2021 valuing the business at $1bn.

The London-based fintech is investing at pace to establish a large claim in the crowded market for open banking payments. Along with its competitors – Tink, Token, Volt, Yapily etc – the company aggregates connections to thousands of banks into a single API. This allows merchants to offer consumers the option to pay from almost any bank through a single connection with TrueLayer. Clients include Cazoo, Coinbase and Revolut.

Although TrueLayer is live 21 countries, it claims market leadership in four – UK, Ireland, Spain and France – and “significant share” in Germany and Netherlands. It has an EMI license in the UK and PI licence in in Dublin.

Management highlight two major product launches.

Variable Recurring Payments (VRP) – TrueLayer was first to market in the UK with recurring payment through its single open banking API as an alternative to direct debit and card on file. Merchants benefit from faster settlement.

Identity data – Signup+ widens TrueLayer’s proposition beyond payment initiation by making bank-sourced identity data available through its API. This simplifies customer onboarding by removing the need for additional verification checks. I used it to sign-up for Plum and can report the customer experience was indeed seamless.

TrueLayer is growing – revenues were up 56% in 2022 and payment volume was 2.8x higher than the previous year – but total sales of £4.14m are modest for a business boasting “annualised total payment volume” of $35bn. As context, a specialist eCommerce merchant acquirer with similar processing volume would be making net revenue of $75m-$150m depending on its risk appetite.

This modest growth has come at considerable financial cost. Administrative expenses were up 88% to £63.4m driven by higher spend on employees – up 99% to £46.4m. Staff numbers ballooned to 434 at an average cost per staff member is £106K. Management trimmed its employee base by 10% at the end of 2022 with the CEO saying “we are now operating in a very different context and more challenging market conditions.”

TrueLayer’s operating loss rose from £31m in 2021 to £61m in 2022. Fortunately, the business is well financed and had £96m net cash at year end.

If shoppers do shift quickly from cards to open banking, the prize for API providers such as Truelayer could be significant. But the market is growing more slowly than many hoped and competition between the specialist players is reported to be ferocious. Consolidation is inevitable and likely to favour businesses, like TrueLayer, with wealthy and committed backers.

Financial results from Yapily show that the open banking market is taking off more slowly than many had hoped. Although Yapily is one of the leading API providers and reported 60% revenue growth in 2022, total sales were less than £3m, generating a modest return on the nearly $70m raised from VCs including Sapphire, Lakestar, HV and LocalGlobe.

European retail banks are obliged to offer APIs that authorised providers can use to access account information or generate account-to-account (A2A) payments. Yapily, founded in 2017 by Stefano Vaccino, a former Goldman Sachs exec, is one of a number of businesses formed to aggregate the APIs offered by thousands of individual banks into a single connection. Although this sounds like a winning proposition, competition is fierce and a number of other start-ups offer similar services. These include Truelayer, Token, Tink, Trust.ly, Nuapay, Volt and many more.

Yapily’s API connects with 2000 banks in 19 countries and, management claims, is accessed by over 3.500 software applications provided by its 500 customers. Yapily has a strong position in providing access to open banking payments for Fintechs, which often use its APIs to offer simple A2A transfers for their customers to top-up accounts. Yapily’s customer list includes Payhawk, Guavapay, Pleo and Quickbooks. The links take you to mini case studies on the Yapily website.

Turnover in 2022 was £2.78m. 80% of sales were the UK, where Yapily is based, but European revenues more than doubled to £0.48m. Management says the positive result was driven “by increased demand as the business expanded into new regions” and stepped up its sales and marketing efforts. Yapily bought a German rival, FinAPI in May 2022 for an undisclosed sum.

The modest increase in topline growth has been costly. Administrative expenses ballooned to £23.7m in 2022 from £9.5m the previous year as management spent heavily on “continued investment in product development, sales and marketing… and support functions as the company scales.” Notably, employee costs more than doubled to £14.6m. Yapily now has 158 staff, mainly in London, costing an average of £92K each.

The team has been busy. Management highlighted a growing range of products, a more extensive network of connections to banks and other financial institutions, a 70% increase in customer numbers and a 4.5 times increase in payment volume. The actual payment volume was not disclosed.

The operating loss grew to £21.5m from £8.4m the previous year, reflecting the company’s “deliberate growth strategy” aimed at “seizing substantial market opportunities” in the emerging open banking market. Accumulated losses now stand at £33m.

Yapily had £18m cash at year end after taking an additional £10m investment. JP Morgan reportedly looked at taking a stake in the business but decided against.

The open banking market is going to be big. The only question is when. And the open question for Yapily and its small army of competitors is whether they can afford to wait.

ParentPay, the UK schools specialist, reported strong a strong increase in turnover in the year to November 2022 although losses widened, mainly due to higher interest payments on its £194m net debt.

The group has leveraged a niche payment business into a strong position in vertical software. Revenue doubled in 2022 to £124m reflecting a full year contribution from ESS, the leading UK supplier of school management software, but also a material improvement in messaging and payment revenues following the pandemic.

In 2021, Montague Private Equity bought ESS from Capita for an enterprise value of £400m. Montague then injected ESS into a ParentPay to create an enlarged group with complimentary payments and software products aimed at Britain’s 30,000 schools. The ESS acquisition didn’t go smoothly. The merger sparked a competition enquiry as school managers protested at a decision to force them to sign three-year software contracts. This combined with a late move to cloud delivery to spark considerable customer churn as this graph produced by Schools Week magazine shows.

ParentPay management say the situation is now under control. The competition authorities have been mollified with additional break-clauses in ESS’s new, longer contracts. And ParentPay will invest £10m into the latest cloud versions of SIMS, its core school software, which it hopes will stem churn and persuade some former customers to return.

ESS was the latest in a series of acquisitions. ParentPay Group now includes 14 companies spanning school management software, kitchen management and cashless catering, all of which generate transactions for the original ParentPay payment processing business. Although 93% of revenue is in the UK, ParentPay is keen to expand on the continent, having acquired WIS in Netherlands, and three businesses in Germany – EDV Service Schaupp (cashless catering), MensaMax and Pair Solutions (both school payment collections).

Post year end, ParentPay has bought two more small businesses – BlueRunner, cashless catering and meal management for £12m, and the assets of CEDAR, a student engagement solution for higher education for £650K. ParentPay sold nimbl, its child debit card, to Caxton for £900K.

The Group now provides services to over 30,000 schools and educational establishments serving 10m students.

In 2022, cost of sales doubled to £105m and administrative expenses rose 121% to £104m including staff costs of £42m. The Group now employed over 1,000 people including over one hundred in sales, at an average cost of £42K each, up 26% on the previous year. EBITDA before exceptionals, the company’s preferred measure of profitability, doubled to £45m.

The original ParentPay school payments business has 11,000 customers in the UK, a market share of a little under 50%, and is highly profitable. Although education is free in Britain, ParentPay collects money for extras including lunches and school trips. Revenue was up 27% to £33m and operating profit grew 13% to £7.5m at a very creditable 23% margin.

Overall, ParentPay Group reported pre-tax losses widening to £18m driven by increased amortisation of acquisition goodwill and higher costs to service the debt incurred with the ESS purchase. ESS was expensive and net debt was £194m at year end, roughly five times EBITDA. Interest expense was £17m, up from £6m in 2021. Management says that cash generation will be used to pay down the debt and, although more acquisitions are on the cards, these are likely to be less ambitions than of late.

Over $600bn has been knocked off the value of the world’s top ten merchant acquirers over the last 18 months. Adyen’s disappointing H1 results only added to the summer gloom surrounding the global payments industry.

While Adyen’s performance was objectively pretty good – revenue up 21% with EBITDA margins of 43% – analysts had been expecting faster growth and took fright at the cost of extra investment in people and product. The stock price which peaked at €2700 in 2021 collapsed from €1700 to just €700.

Adyen bulls point out that the Dutch acquirer/processor is strong in Europe where the level of payment complexity delivers consistently higher margins than the US. And its growing POS business sets it apart from online focused processors such as Stripe and Checkout.

But Adyen has suffered badly in North America where a price war is raging among large acquirers competing for business from large digital merchants. One beneficiary has been PayPal which is reported to be hoovering up volume via its Braintree brand at a margin of less than 2c per transaction.

Of course, the collapse in value isn’t restricted to merchant acquirers. Fintech is generally under the cosh. Is it an apocalypse? No, says Ben Robinson, who argues manufacturing and distribution of financial services will continue to separate, opening a significant opportunity for embedded finance sold to merchants via ISVs, some of which now generate >60% of revenue from payments.

Analysis from Sifted Research records a sharp fall in new Fintech finance rounds. Start-ups now have no choice but to prioritise conventional business metrics such a cashflow and margin. “The familiar VC growth strategy — losing money for years to acquire new customers — is not a winning pitch right now.”

Following the announcement of the $610m purchase of the less interesting parts of PayU, Arik Shtilman, Rapyd’s colourful CEO, gave a long interview with FXC revealing that the combined business will process $120bn payment volume from 250,000 clients and generate revenues of c.$1bn. This is only the start. Shtilman maintains that Rapyd will hit $2bn revenue and $400m EBITDA by 2026. We’ll be following this very closely.

dLocal, one of the small group of cross-border merchant payment specialists which competes with Rapyd, may be up for sale. Trading through a UK company listed on NASDAQ, regulated in Malta and with an HQ in Uruguay, dLocal has shrugged off a short-selling attack and a fraud probe to post annual revenues of c.$600m. Rapyd would certainly be interested. Maybe Worldpay too.

Like Don Quixote tilting at windmills, EVO is not giving up on its €1bn damages claim against Santander. It alleges the Spanish bank failed to deliver enough sales leads. The American acquirer, now owned by Global Payments, is appealing a lower court decisionin favour of Santander. Meanwhile, Universal Payments, EVO’s Spanish unit, is being merged into Commercia, Global Payments’ joint venture with La Caixa.

Despite the global dominance of Visa and Mastercard, there’s plenty of life in domestic payment schemes. In this short review, Edgard Dunn counts 90 of them, including many in Europe. Germany’s Girocard reported volumes up 15% in H1 2023 and Blik, the wildly successful Polish mobile payment standard, announced eCommerce volumes up 42%

In contrast, Carte Bancaire, the long established French domestic scheme is losing ground to the international brands. Some French banks have stopped co-branding their Visa/Mastercard cards with Carte Bancaire and the consumer preference for Apple/ GooglePay has stimulated usage of the international brands.

Maybe that’s why Instacart, the leading US player, is expanding deeper into the grocery value chain with technology and data products. It bought Caper, a smart cart vendor for $350m in 2021. Schmucks is the latest retailer to adopt the carts, commencing with 10-20 in each store.

Smart carts make a humane alternative to the self-checkout machines that are making people lonelier. Trader Joe’s CEO pledged never to replace employees with machines, saying “I have fun bagging groceries and working at the register. Self-checkout is work. I don’t want that.”

Turning to biometrics, it seems Amazon One, the retail giant’s new palm-payments product, is about more than shopper convenience. It’s part of a plan to own a central ID verification system that would help Amazon compete with Google and Apple. Amazon One uses generative AI. Obviously.

Payface, a Brazilian start-up, says its facial recognition payment product will be in 2,000 supermarkets by the end of 2023. The company just raised an extra $3m following a $6m funding round last year.

There’s nothing more dispiriting than a long queue of cars at a drive-through coffee shop. Starbucks is experimenting with geo-location so people can just pick up their coffee from the hatch and be on their way.

Subscription commerce

New academic research analysing card transaction data shows customer “inattention” boosts subscription revenues between 14% and 200% depending on the merchant. No wonder regulators are beginning to show an interest in helping shoppers terminate unwanted subscriptions.

Payment providers need to be alert to scammers that dupe consumers into signing up for bogus subscriptions. PayOne, Worldine’s German eCommerce payment business, has been banned from onboarding new high-risk customers. The regulator is unhappy that PayOne had been processing transactions linked to fraudulent subscriptions, phishing and fake stores.

Similarly, ING is being sued for €14m lost by investors defrauded by customers of Payvision, the PSP acquired by the Dutch bank in 2018 for €375m. The Dutch central bank has said that Payvision deliberately ignored signals about fraud from its clients. ING was obliged to close Payvision business and write off the purchase price.

And fraud is getting easier. Why build your own criminal infrastructure when you can use scam-as-a-service to create phishing or fake advertising content? The product, available via Telegram, even includes a payment gateway and price optimisation tools.

Car Commerce has long been a focus for payment innovation but has delivered little useful product to show for the effort. BMW has abandoned its second attempt to sell heated seats on subscription. Customers were angry at paying to turn on a feature in a car they’d already bought. A BMW director commented: “People feel that they paid double – which was actually not true, but perception is reality.”

Pace Drive and ryd, two German start-ups developing alternative payment apps for buying petrol seem to be struggling. Commentators point to the declining market for auto fuel and the high cost of customer acquisition. Undeterred, Henderson has introduced a Fuel Pay app targeted at independent service stations in the UK that can’t or won’t afford outdoor payment terminals.

Payment apps make more sense for supermarkets which can use them to integrate complex loyalty programs into a simple checkout experience. Rewe, the German grocer, is ditching Payback, a 3rd party loyalty programme, and launching Rewe Pay in 2024.

Two small UK acquirers made interesting announcements. Acquired.com has launched a hosted checkout including cards, alternative payments and open banking delivered through one integration with a single regulatory license. The company says this is a world first. Any readers disagree?

Ecommpay has launched US acquiring and chargeback insurance. 3DS is still optional for US merchants, resulting in chargeback rates of 4.3% for Ecommpay’s customers. Its new solution would see this fall to just 0.5% although merchants will need to pay additional transaction fees.

Digital receipts should be a standard component of any modern POS bundle. These are cheaper and better for the environment than paper. And there’s always the chance of capturing customer contact data. Verifone has partnered with Receipt Hero, with which it was already working in the Nordics.

Pi-xcels, a Singapore start-up which has invented a simple way of pushing digital receipts to shoppers’ smartphones, has raised $1.7m seed funding. Ingenico is already distributing the product and here’s a short demo that shows how it works. I’ve met the management. They’re an impressive bunch. Let me know if you’d like an introduction.

Merchant cash advance involves lending money to small businesses secured on card payment receipts. Some new vendors are making an impact. Keep an eye on PragmaGo which is working with Polksi ePłatności, Poland’s second largest acquirer. It charges 18.5% for a 12 month loan. Also Flowpay from the Czech Republic, which operates a whitelabel model with leading central European ISVs such as Shoptet and Storyous.

In the UK, YouLend, a finance house is winning a good share of partnerships at the moment, including working with Amazon.

SoftPOS

Polcard, Fiserv’s Polish unit, has equipped 4,900 DHL couriers with Polcard Go, its SoftPOS product. DHL says the main benefits are removing the need to carry a separate payment terminal to take payments from shoppers on the doorstep, no worrying about cables/chargers and the elimination of paper receipts. DHL’s comments back up a new survey from RS2, a payment software vendor with a SoftPOS solution, that “ease of use” rather than saving money is the main driver for merchants adopting the new technology.

Oona, a Finnish hardware vendor, is taking advantage of this growing interest in SoftPOS from large retailers. It has launched a range of Android self-service kiosks with can be enabled to take payments using SoftPOS applications. Here’s an example working with Viva Wallet, the Greek Fintech owned by JP Morgan.

Apple has launched SoftPOS in the Netherlands, its second European market after the UK. Adyen and SumUp are the launch partners. SumUp is charging 1.69% with no monthly fee.

In vendor news, Trustly is looking a likely winner in the forthcoming open banking shake out. It has bought SlimPay, the French account to account payment specialist for a reported €70m. SlimPay brings €5bn volume, a good subscription payment platform and a useful presence in France.

Berlin based Ivy has raised $20m at a reported $80-90m valuation only five weeks after making public its initial $8m seed round. Ivy plans to build an international network of open banking APIs. The CEO makes a bold claim: “Ivy is building for account-to-account what Visa and Mastercard have built for card.” If you’re thinking this sounds a lot like Volt, it does.

Klarna launched Klarna Kosma in 2022 which brought the BNPL giant’s internal scale to the provision of open banking API aggregation in competition with Token, True Layer and others. Klarna announced it was axing the Kosma brand before clarifying that it wasn’t. Klarna says that banking API aggregation sales to 3rd parties have tripled in the past year but disclosed no numbers.

Cash

India has hit its goals for 80% financial inclusion in just six years by investing in digital infrastructure according to a new OECD report. The study also praises PIX, the very popular Brazilian mobile payment scheme (see graph below). Both countries see moving everyday commerce from cash to digital payments as key to combatting financial exclusion.

In contrast, campaigners in developed economies focus on retaining access to cash, even at the expense of higher charges for small businesses and shoppers. Many US cities are passing laws obliging businesses to accept cash. Los Angeles could be the latest. Trends include “reverse ATMs” which turn cash into pre-pay plastic, often associated with high user charges, or for merchants to direct customers to withdraw cash from a captive ATM in store. These often charge upwards of 3.5% commission, as Dave Birch found out in New York..

GB News, a right-leaning TV station, organised a petition signed by 300K people demanding retention of cash in the UK. In response, the British Government has pledged that banks will be obliged to ensure customers can find a free ATM within three miles of where they live.

Central Bank Digital Currencies (CBDC) might seem attractive as a means of keeping both sides of the argument happy. It’s cash. But it’s also digital. What’s not to like? Digital dollars or euros would leap from your wallet to the merchant’s wallet without touching the banking system. The Bank of England has launched a consultation on the digital pound which outlines this very unexciting use case. I’ll stick with my debit card, thanks.

Crypto corner

Checkout.com has stopped providing card processing services to Binance, the world’s largest crypto exchange citing concerns over Binance’s anti-money laundering, sanctions and compliance controls. From a peak of $2bn in 2021, monthly volumes processed by Checkout for Binance had declined to “just” $300-$400m. Reports suggest Binance insisted on disabling 3DS resulting in “a European organized crime syndicate [taking] full advantage.”

Customers flocked to Binance in 2021 to take part in the NFT bubble. People lost their heads exchanging dollars for ethereum so they could “buy” jpgs such as the Bored Apes, These were auctioned by Sotheby’s at an average price of $241,000 each. The monkey-themed NFTs are now worth rather less. Disappointed punters are suing the auction house claiming it had “given an air of legitimacy… to generate investors’ interest and hype around the Bored Ape brand.“

Remarkably, there is still some investor interest in crypto payments. CityPay, from Georgia, has just raised €2m for its crypto/fiat gateway.

I know I’m a sceptic but if crypto is ever to become a mass-market payment instrument, the industry needs to address the user experience. Last month, one Bitcoin user accidentally paid $500,000 in fees to make a single transaction. Complexity seems a feature not a bug.

Stablecoins, sometimes referred to as “backed” crypto are certainly less risky. Indeed, some believe PayPal’s digital dollars (backed 1:1 with US Treasuries) are safer than the real thing. Getting acquirers involved seems sensible too. Visa is piloting USDC stablecoin settlement with Worldpay and Nuvei.

NCR, the retail tech and ATM vendor, is splitting in two. The retail business will be called NCR Voyix. The “x” represents “the actionable insights delivered to customers and the visual manifestation of the company’s ability to ‘link’ the digital and physical worlds”. That’s a big ask for just one letter. The ATM business is to be renamed NCR Atleos, a portmanteau of At (automated teller) and eos (the Greed goddess of the dawn).

Belgium’s economy minister has proposed to reduce debit interchange below the 0.2% ceiling imposed by the EU’s MIF regulations. The local banking association is not happy.

Ken Serdons, Mollie’s COO, gives an interview. The Dutch company’s success as “the most loved payment provider” in Europe is all about the onboarding, he says. Meanwhile. Mollie, which lost €120m last year, is making its first layoffs. Adrian Mol, CEO, said “we hired too many people in a short time and went too far. The company is no longer efficient.”

Swish, a P2P payment app, is used by 92% of Swedes. Here’s a good piece explaining why it has grown so quickly. Although market research showed people would pay for the service, there was a massive backlash against user charges when it launched. The product is now free.

Wirecard latest. Here’s a full round up from the FT of court proceedings in Germany and Singapore. According to the paper, no witness has yet presented hard evidence that Markus Braun, CEO, was aware of the fraud. Equally, there seems no hard evidence that he took the allegations seriously when brought to his attention.

And finally

“When I want a Whopper, I want it now.” It’s 1993 and Burger King starts accepting credit cards.

Where to find me?

I’ll be at Open Banking Expo in London on 18-19 October and at MPE 2024 in Berlin on 12-14 March. MPE has gone all pop-art this year. I don’t normally look this flourescent.

Miura Systems, a small UK based payment terminal vendor, reported good numbers for 2022 after having been badly hit by the pandemic. Turnover was up 60% to $27.4m powered by particularly strong recovery in the Far East.

Miura’ Shuttle and M10 products were ubiquitous in the early 2010s as the company was one of the first to market with mPOS devices. The strong focus on design brought by Enrique Garrido, its founder and majority shareholder, was refreshing and the company still has “beautifully simple, innovative” in its mission statement. Garrido has since stepped back from day-to-day management which is now in the hands of Executive Chair, Andrew Dark.

The company is very reliant on its customers in Asia Pacific, served from a sales office in Japan. Asia Pacific revenue was 84% to $21.9m. Growth in EMEA was more modest, up 16% at $5.1m, while sales in the Americas continued to decline to just $0.3m. Management says it now has renewed focus on EMEA and Americas with the new Miura Android SmartPOS terminal believed to be the key to success.

A second key focus is growing services revenue. Revenue from services remains small but more than doubled to $0.628m. This gives the support of recurring licence and transaction based revenue to balance the traditionally rather lumpy hardware business.

Overall, the company seems confident, stating that the new order book is strong and at its best position since 2019.

Although sales are back at pre-pandemic levels, profitability is not. Margins have been squeezed by ongoing supply chain disruption and inflationary cost increases on components. Gross margins picked up a little to 28.4% but remain well below 2020 levels. Miura says it has increased its sale prices and believes that margins will bounce back com the medium term.

Management has controlled costs very well. Administrative expenses fell 16% in 2022, helping Miura return to the black with an operating profit of $1.35m. The operating margin of 5% is, again, well below the 10% levels recorded before the pandemic, but gives confidence for future investment.

AIB Merchant Services, the Irish joint venture between Allied Irish Banks and Fiserv (First Data) reported a strong performance in 2022 with profits up 31%.

Dublin based AIBS is Ireland’s largest domestic merchant acquirer. It serves all business types, large and small, with lead generation primarily via the bank network. The product portfolio includes Clover and the business competes with Bank of Ireland Payment Acceptance (Global Payments) and Elavon.

In the UK, AIBMS mainly supplies SMEs through ISO relationships such as Fidelity Payment, Card Saver, CardcuttersAdelante and Payment Plus. Post-Brexit, AIBMS can no longer serve its British clients from Ireland and has established a UK entity which is expected to receive its payment institution licence during 2023.

The third leg of the business is internationally focused and high-risk with domain expertise in gambling and gaming. AIBMS can pay out in 18 currencies and offers multi-functional Merchant IDs (MIDs) which greatly simplify multi-currency and multi-channel operations for complex merchants.

The company’s focus in 2022 was “managing merchant charge back risk and negative balance risk” arising from the pandemic and the economic recovery. This was successfully achieved although management report “some inflationary pressures but no slowdown in merchant sales.”

AIBMS does not report payment volume but does disclose gross fee and commission income – the total amount it billed to merchants including interchange and scheme fees. This figure grew 44% to €780m with particularly strong performance in Ireland which remains the company’s largest market. Although merchant service charges grew 41%, revenue from other fees which includes terminal rental was up just 8%.

Management points to to “economic activity returning to pre Covid-19 levels” and the continued consumer shift from cash to card. Volumes also benefited “substantially from the boarding of large corporate merchants via wholesale independent sales organisations” such as Payzone, the Irish ISO acquired by AIB and Fiserv for €100m in 2019.

Net fee and commission income – after deducting the changes passed through to the card schemes – rose rather more slowly, and was up 16% at €112m. This likely fall in take rate could be due to a growing proportion of enterprise customers in its portfolio or an unfavourable mix of transactions processed by customers on fixed price contracts. Or both.

Operating expenses rose 13% to €57m. Total staff costs were up 16% to €12m. Employee numbers grew from 108 to 135 at an average of €91K each. Credit losses grew 23% to €2.1m or 1.9% of net revenue, modest for a business with a number of high-risk clients.

Net operating income grew 31% to €62m with operating margin up 7%pts to 55%.

Unlike Cardnet, Fiserv’s JV with Lloyds Bank in the UK, AIBMS is still not paying a dividend to its parents “due to the potential for chargeback loss events arising” from the pandemic and “the uncertain economic outlook.” However, AIBMS has made a €75m loan to Fiserv at commercial rates.

")