Four years ago, I wasn’t convinced Santander could turn a collection of disparate payments assets into a coherent platform but the latest results suggest it has done exactly that. Santander is now a rare European bank making a success of merchant payments, delivering consistent growth and rewarding shareholders with eight successive quarters of profitability.

It’s not been an easy journey. Santander first put its payment assets together in 2020 under the PagoNxt brand and bought Wirecard’s tech platform and Munich operations. The result: an alphabet soup of brands and €170m write-offs.

The business is much clearer now. PagoNxt has been renamed Santander Payment Solutions and consists of three divisions:

Getnet merchant acquiring, active in Iberia and Latin America

Getnet Platforms, including A2A and Santander’s issuing processing which services the group’s retail businesses in Brazil, Mexico, Chile, Spain and the UK

With 1.2m merchant customers, Getnet is the division that most interests readers of Business of Payments. Getnet Payment volume grew an impressive 17% in Q2 to €67bn, and has roughly doubled since 2021.

Getnet offers a single API to connect to its Latin American markets which helps international merchants easily navigate multi-market entry. This was one reason for improved performance in Mexico and Brazil. The latter despite the rapid growth of PIX, which has yet to make a meaningful dent in card acquiring.

Recent product enhancements include “Pay In” for Brazil which allows international merchants to receive payments without establishing a legal entity in the country, DCC in Mexico and white-labelling AEVI’s POS platform (initially in Mexico) which will help secure business from large retailers.

The total number of transactions, including both Getnet acquiring and Getnet platforms, rose to 8.6bn in Q2 26, up 48% year on year, largely driven by increased A2A activity in Brazil. This number may well be associated with PIX.

Santander management has highlighted the importance of scale in driving down unit costs. This strategy is working. Cost per transaction for the half year was 1.6c compared with 2.9c a year ago and 3.6c in 2024.

The improved unit economics has begun to flow to the bottom line.

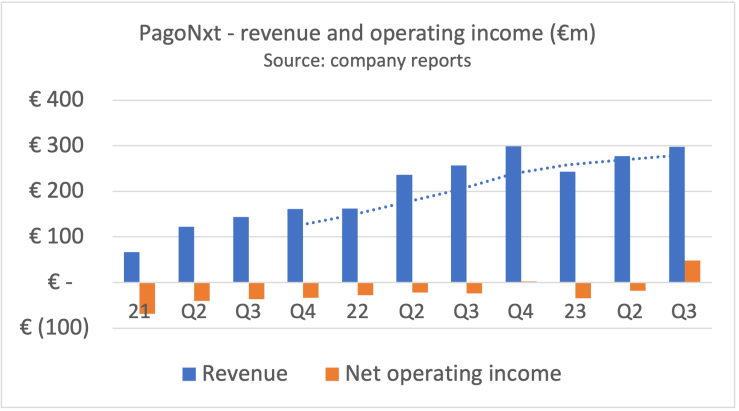

Net revenue grew 19% to €387m, expenses were up 16% to €337m reflecting continued platform investments and net operating income rose 46% to €51m. The operating margin is a very respectable 13%. Cash performance is even better. Santander Payment Solutions generated EBITDA of €123m in Q2 26, a healthy 32% margin.

Santander has proved it can build a profitable merchant acquiring platform. The next challenge is to turn Getnet from a regional champion into a genuinely pan-European proposition. That means expanding beyond its traditional Iberian and Latin American strongholds and strengthening its merchant offering in markets where the bank has a major presence such as the UK and Poland.

Santander reported that both volume and revenue growth at PagoNxt were the slowest since the business was formed in 2020. PagoNxt groups the bank’’s payment capabilities in single operating division but Santander has struggled a little to mould these businesses into a coherent whole.

The German merchant acquiring business and Superdigital, its Brazilian subprime unit were closed in Q3 at a total cost of €243m. Next to leave will be Ebury, although in happier circumstances. The UK-based trade finance specialist is set to float on the London market in early 2025 at a valuation of around €2bn.

This will leave PagoNxt with two divisions. The largest is Getnet, a merchant acquirer with strong positions aligned to Santander’s domestic banking network – Spain, Portugal, Brazil, Mexico (where Getnet launched contactless ticketing on the Mexico City metro) and Argentina. Getnet is the number two acquirer in Latin America and will start selling in Chile shortly. The Latin American capabilities are now available to merchants through a single API connection called Getnet SEP (single entry point) which will be attractive to European merchants looking to simplify acceptance in this part of the world.

Total merchant payment volume at Getnet was up 7% in Q3 to €57.6bn with the strongest performance in Mexico, Spain and Portugal.. ATV was up 3% at €23.03.

PagoNxt Payments, sometimes known as Payments Hub, will be PagoNxt’s second operating unit. PagoNxt Payments groups all Santander’s A2A capabilities. The bank is steadily migrating its operating units onto the new platform and transaction volume is reported to be 5x greater than a year ago.

Total revenue across all today’s Pagonxt divisions – Getnet, PagoNxt Digital and Ebury – was up just 4% at €311m in Q3, the lowest growth since the division was founded four years ago. In better news, the proportion of business sourced from outside the Santander banking network has reached 24% year to date. This has grown from 14% in 2022 and is a key metric to help judge whether PagoNxt can prosper independently.

Expenses rose 15% year on year to €288m. Management believe technology spending has peaked and it’s now a question of driving down unit costs by driving up volume. There are early signs that the strategy is working. Cost per transaction processed, in constant currency, continues to fall and was down 7.5% YTD at 3.6c. This number includes acquiring and A2A.

Operating income, quite volatile from quarter to quarter, was down 52% at €23m in Q3 but flat year to date.

EBITDA margins were up 3.1pp to 23% YTD and management is confident of hitting its medium-term target of 30%. This seems achievable on the current trajectory, but management is also sticking to its 30% revenue growth target. This seems more ambitious – revenue was up just 12% YTD – and will present an early challenge to Juan Franco, the newly appointed PagoNxt CEO who joins from Nuvei.

Significant write-downs at PagoNxt, Santander’s merchant payment business, masked a good underlying performance reported with the bank’s Q2 2024 financial results. Notably, economies of scale in payment processing helped double EBITDA to €69m.

PagoNxt was created when Santander consolidated its payment assets into a single unit containing Getnet, a multi-national merchant acquirer, Ebury, a London based trade finance specialist, Superdigital, a Latin American financial marketplace for the economic inclusion of the underbanked and PagoNxt Payments which offers wholesale A2A capability based around its Payments Hub.

The refocused Getnet is the second largest acquirer in Latin American and has good positions in Spain and Portugal where it sells through Santander’s large domestic banking networks. Santander also has a strong footprint in the UK where Elavon is the bank’s preferred payment partner today. It’s not clear if or when Getnet will replace Elavon in this relationship.

Returning to the Q2 2024 results, global merchant payment volume at Getnet rose by 9% to €54bn. This is the slowest increase in volume yet reported by PagoNxt and reflects the impact of the loss of its German merchants. ATV ticked up 6% to €20.85.

Payments Hub which offers a single API connection into a number of A2A platforms including SEPA, Faster Payments and SWIFT, is growing fast from a low base. Total transactions increased from 79m to 405m in the first half of 2024.

PagoNxt is successfully turning increased volume into sales revenue. Turnover was up 8% to €300m with the good performance attributed to Getnet in Europe, Chile and Mexico, where it deployed DCC for the first time, as well as higher sales at Ebury.

Management is keen to reduce its dependence on Santander and was pleased to report that 22% of total PagoNxt revenue is “open market”, that is sourced from its own distribution, compared with 14% last year.

Higher volumes have begun to deliver economies of scale. Unit transaction costs at Getnet fell 9% to 3.7 cents, allowing operating expenses to hold steady at €297m despite the growing size of the business.

PagoNxt is now consistently profitable on an underlying basis. EBITDA doubled to €69m in Q2 as the margin grew 8pp to 20.1%. Management believes that it is on course to reach the medium term target of 30% EBITDA margins.

Net operating profit before the write downs was €4m compared to a loss of €18m in the same quarter of 2023. After the write downs, PagoNxt lost €258m.

PagoNxt, Santander’s payment unit, saw the benefits of platform consolidation and economies of scale as it announced a second successive quarter of strong profits in Q4 2023. Reporting 25% EBITDA margins, management says that higher profits are primarily due to increasing scale, increased VAS penetration, and a greater share of eCommerce and vertical solutions.

Ana Botin, Executive Chair of Santander said: “We have a unique position.We are on both sides of the value chain. We will use this to become a global leader in payments… We’re driving customer growth by offering a bundle proposition.” This is a claim which most banks could make but Santander is one of the few making a success of the strategy.

The very positive Q4 financial performance follows Santander’s decision to in-source and consolidate its payment activities. PagoNxt comprises all of Santander’s payment assets, including Getnet, a leading multi-national merchant acquirer, Ebury, trade finance, Payments Hub, “already one of the largest processors of A2A payments in Europe” and Superdigital, a financial marketplace for the economic inclusion of the underbanked.

Total merchant payment volume at Getnet was up 19% to €57bn with strongest growth in Europe where volume rose 31% year on year, driven by good results in Spain and Portugal. In the UK, Getnet is “currently operating with a reduced number of customers under our UK FCA licence.” Management says that Getnet Europe has introduced a new vertical solution for airlines and stronger value-added propositions for SMEs.

Mexico volume was up 23% with Brazil growing more slowly at 14%. The new business in Chile increased volume 80% from a low base. PagoNxt says it is now the third largest merchant acquirer in Latin America.

For 2023 as a whole, volume was €206bn, up 22%. Total transactions increased 29% although PagoNxt has stopped reporting the actual number.

Revenue rose 7% to €321m, due mainly to higher merchant volumes at Getnet and strong performance at Ebury. PagoNxt is tasked with growing its business outside of Santander’s banking relationship. 15.8% of revenue in 2023 was “open market”, up 2.2 percentage points on 2022.

Expenses fell 9% to €268m. Payments carries high fixed costs.. As volume has grown, the cost per transaction processed at Getnet fell 16% in 2023 to 3.5c.

Net operating income was €53m, up from €3m same quarter a year earlier, yielding an impressive operating margin of 17%. The EBITDA margin was 24.8% (up 15.7pp on 2022) and management is confident of hitting its 30% margin target by 2025.

Looking ahead, PagoNxt management is focused on scaling its global platform, strengthening distribution through Santander especially to SMEs and maximising the “open market” opportunity through partnerships with ISVs and financial institutions.

Lifting the gloom a little, PagoNxt, Santander’s payment business, reported sparkling Q3 results including a maiden operating profit. This performance highlights the success of Santander’s decision to in-source and consolidate its payment activities. PagoNxt comprises all of Santander’s payment assets, including Getnet, a leading multi-national merchant acquirer, trade finance expert Ebury, Payments Hub which brings together the bank’s account to account transactions, and Superdigital, a financial marketplace for the economic inclusion of the underbanked.

Q3 merchant payment volume was up 27% to €54bn “backed by good merchant performance” in Mexico, Brazil, and Europe and share gains in all core markets. Transactions grew 26%, leaving ATV steady at €22.46.

Management gave few other updates but said that the Payments Hub is “already one of the largest processors of A2A” in Europe and is now processing transactions from Santander businesses in Spain and the UK.

Overall revenue was up 16% in Q3 to €298m but expenses fell 11% to €251m. It’s not clear what has led to the decline in operating costs but the impact on operating profits was very positive. PagoNxt reported an operating profit of €48m for the quarter at a healthy 16% operating margin, compared with a loss of €24m in 2022. It will be interesting to see whether this is a blip or the first step towards steady growth in profitability.

One of the key reasons for the collapse in Worldpay’s valuation is that when FIS bought the business, it was growing sales at about .9%. However, starved of funds under FIS’s ownership, Worldpay hasn’t been able to keep up with high-spending competitors such as Adyen, Stripe, Checkout and JP Morgan. The result: revenue was up just 1% in Q2, JP Morgan has overtaken Worldpay to the global number one spot and $25bn has disappeared.. More details on the Business of Payments blog.

In Europe, most attention is focused on battles for bank partnerships. In Italy, Banco BPM, advised by Bain Consulting, rejected its current partner, Nexi. Instead, in a surprise move, the Milan bank will merge its merchant services business with that of BCC Pay. The combined group, boasting 370,000 POS and €90bn volume, will claim number two spot in the Italian market and has the scale to compete with Nexi and Worldline.

Two other large European banks are in the process of finding partners for their merchant services arms. In France, Credit Agricole has now signed the agreement with Worldline to start a new JV. The revenue should start to flow in 2025. Again, there was less positive news for Nexi. The closure date for its acquisition of a majority stake in Sabadell’s merchant acquiring business (the second largest in Spain) has been put back six months to the first half of 2024.

Both Worldine and Nexi’s merchant services businesses themselves, seem in good underlying health. Reporting H1 results, Worldine revenue was up 13%. Management said it was still interested in acquiring merchant portfolios from banks. Nexi grew revenue 10% in H1 and is proving adept at realising synergies from the recent mergers with SIA, Nets and Concardis. It has decommissioned five of 25 processing platforms, says it’s on track to close another five in H2 and, longer term, to reduce the number to just four.

PagoNxt, Santander’s payment business, is also doing well. Volume was up 22% in Q2with increases recorded in all major markets in Europe and Latin America.

We’ve reported previously on the challenging market conditions for pure-play eCommerce gateways. It’s no surprise that privately owned Computop, which claims 30% of the German eCommerce market, has sold a 30% stake to Nexi. There is strategic logic for Nexi which already owns Concardis, Germany’s largest acquirer. Computop’s volume processed fell from €34bn in 2021 to €30bn in 2022. The decline is partly due the company’s decision to exit the gambling/adult sectors but also indicates competitive pressure from Adyen, Checkout and Stripe.

The decline in value of German payment assets was underlined by KKR’s decision to hand Unzer (formally HeidelPay) to its creditors, writing off most of its $668m investment. KKR acquired a majority stake in Heidelpay, a PSP with about 17% of the German eCommerce market, in 2019. Unzer was recently in trouble with BAFIN, the German financial regulator, due to “serious defects” in its risk processes.

US based Shift4 still hasn’t concluded its acquisition of Credorax Finaro, a European processor. First announced in March 2022, the deal hit regulatory obstacles linked to a sanctioned Russian oligarch on the Finaro share register. Management says it is confident of closing the deal in Q4.

Ryan Reynolds is a much better proposition as shareholder. After taking an undisclosed stake in Nuvei, a Canadian processor with global ambitions, the actor is fronting a witty and self-deprecating brand advertising campaign. Reynolds’ investment is already under water. Nuvei’s stock fell 39% after disappointing Q2 results.

Rapyd, the London based global “fintech as a service” provider, has paid $610m for the slowest growing and least profitable parts of the sprawling PayU empire. The purchase price will be financed by a fresh capital injection into Rapyd in what the company claims could be the largest Fintech fundraise of 2023. Arik Shtilman, CEO, took to LinkedIn to explain the rationale. “If you don’t aim for a big outcome, you won’t get an outsized return,” he says. More details on the Business of Payments blog.

We reported last month that Toast, a leading US restaurant software vendor with integral payment processing, had shocked its merchants by adding a $0.99c service charge to each bill. The fee would have been paid by diners and provide Toast with free money at 100% gross margin. The company has now back tracked with its CEO recognising “we made the wrong decision.”

Shift4, with time on its hands waiting for the Finaro deal to close, responded with a clever “Don’t get Toasted” campaign.

Synch Payments, an attempt by a consortium of Irish banks to produce a domestic mobile money transfer app to rival Revolut, has been delayed once more. Again, it’s Nexi supplying the technology.

While autonomous stores are gaining traction across Europe, Amazon, which invented the technology, is struggling. According to the RTHI blog, Amazon’s stores are in the wrong place, have the wrong products, cost too much to build and are confusing for customers. For example, you can now checkout by tapping your physical payment card but not with Apple/Google Pay. Or with Amex. The stores don’t even accept Amazon gift cards.

Customer satisfaction with traditional self-checkouts is falling. Shoppers resent the ongoing reduction in staffed checkout. With autonomous stores so expensive, smart carts may provide a cheaper and more flexible compromise. Here’s a good round up from Forbes on the state of play. Kroger, the US grocer, says smart cart shoppers spend less time in store but spend more money. Everyone’s a winner.

Shoppers are returning to local stores. As expected, once confronted with the true economic cost of rapid grocery deliveries, people are willing to walk to the shops just like it’s 2019. The last mile delivery specialists are disappearing one by one. Getir is the latest to urgently need more cash to keep trading. Maybe robot deliveries are the answer.

Fans of biometric payments will be delighted that Amazon is rolling out Amazon One, its palm payment product, to 500 US Wholefood stores by the end of this year. Amazon says the technology has been used 1m times to date with zero false positives and is ideal for high volume locations such as stadiums. Shoppers first need to visit an Amazon One location where they can scan their palm and link it with their Amazon account.

Palm payments are no more convenient for shoppers than Apple/Google Pay. But there is clear benefit to Amazon of capturing extra customer data and/or being able to steer transactions to lower cost payment methods.

While Amazon can probably be trusted to keep your data safe, other vendors may not be so reliable. For example Worldcoin, a San Francisco-based start-up, is creating a global identity database founded on iris scanning and secured $115m funding in May this year. Its focus has been mainly on developing countries such as Kenya, in which Worldcoin has been asking people to agree to having their eyeballs scanned in return for $50 in tokens on the blockchain. What could possibly go wrong? Bain Capital is one of the VCs which should know better than be mixed up in this madness.

Product

Legacy acquirer like Worldpay and Barclaycard need to make rapid product investments to keep up with the new capabilities showcased by Adyen, Checkout and Stripe.

Optimised checkout is a great example. This uses AI to configure checkout pages with the best selection of payment brands, ensures that transactions contain the correct data and optimises routing to maximise acceptance or minimise cost. Stripe claims merchants moving to its optimised checkout grew sales revenue 10.5% more than a control group which stayed on the old product. Checkout says its Intelligent Acceptance product increased acceptance rates by up to 9.5ppts. Early customers include Klarna.

Checkout.com has also launched Identity Verification which, it says, uses AI to identify individuals within 120 seconds as they video themselves holding up identity documents. Uber Eats is an early customer.

Adyen announced Data Connect for Marketing which helps merchants identify their in-store customers. Retailers used to this themselves before PCI regulations banned them from storing customers’ card details in their own systems. Impressively, Adyen is also the first Fintech to join FedNow, the new US instant interbank payment network.

Subscribed

Away from the global processors, Cashflows, a UK eCommerce acquirer, has added a range of Castles POS terminals as part of omni-channel proposition to its ISV and ISO distribution partners. This is a smart move. New UK regulation has outlawed lengthy POS terminal rental contracts but were connected to one of the 14 largest acquirers. Cashflows is not one of the 14 and so will be an attractive option for ISOs looking to continue business as usual.

Far Eastern tourists are back in Paris to shop and the top retailers know they need to offer their favourite ways to pay. Printemps, a leading department store, has integrated Alipay+ into its POS checkout flow. Alipay+ also gives access to Kakao Pay (South Korea), GCash (Philippines), Touch ‘n Go (Malaysia) and TrueMoney (Thailand).

Fuel cards are commonly issued to staff who drive company vehicles but there’s always a risk of fraud or misuse. A new idea from CarIQ uses vehicle data as a sort of biometric ID. Linked to a virtual card, the vehicle pays for its own fuel, without the driver needing to sign for the gas. CarlQ has just signed a global partnership with Visa.

Access to cash

As cash usage declines, a growing number of merchants are only accepting digital payment. This presents problems in societies where some citizens don’t have access to electronic money. But cash-free stores are also enraging many of the people already angry about vaccines, traffic restrictions, 5G masts and sundry other inevitable aspects of modern life.

If cash is to be preserved, public policy needs to address the fact that the less cash is used, the more expensive it gets. For example UK convenience stores often host ATM machines with the retailer receiving a commission of 15p per withdrawal. One store reports transactions down 70% at a “free” ATM. The result: the retailer is not making enough revenue and is switching to an ATM that charges customers a withdrawal fee. The likely outcome is that transactions will fall further.

SoftPOS has only been available on Android so news of the European launch of Apple’s “Tap to Pay” on iPhone made the headlines. Apple’s SoftPOS is based on the $100m acquisition of Montreal-based Mobeewave in 2020. Architected differently to Android SoftPOS, Apple offers an SDK to developers/PSPs allowing them to build payment acceptance capability into their own iPhone apps.

With Apple SoftPOS, there’s still a need for an acquirer (or payment facilitator) to process the transactions but no obvious role for the specialist payment app/gateway providers such as MyPinPad or Phos. Happily for the SoftPOS start-ups, the Android market is large enough to keep them all busy for some time.

In Android product news, Oona, a Finnish start-up, has some interesting enterprise SoftPOS ideas such as this kiosk, for which Rubean provided the payment application. Getnet (Santander) has launched SoftPOS in Spain although only for larger business customers. Finally, Worldine is now live with SoftPOS in Italy via its new Banco Desio partnership supported by a clever TV commercial.

Open banking

Natwest, which has modestly taken the URL www.bankofapis.com, commissioned a report to identify the key obstacles holding back the wider adoption of Open Banking. It concludes the problems lie in “lack of commercial incentives” to develop or enhance the core APIs and “lack of alignment between.. .banks.” Or as Nick Dunse, former CMO of Pay with Bolt wrote on LinkedIn, “Nobody is leading it and there’s no money in it.”

Some Fintech lobbyists are asking the regulator to lead by expanding the number of services available but Oliver Wyman, the management consultant, thinks its time for banks to introduce financial incentives for themselves by monetising the APIs. The consultants suggest that a typical bank could make $50-$75m per annum if it charged PSPs for value added services linked to the open banking APIs.

Variable recurring payments (VRP) – an open banking equivalent to direct debits – were meant kick start the sector in 2023 but have also been rather slow to take off. Here’s a good podcast from Edgar Dunn which explains how VRPs work and what the opportunities might be.

In corporate news, NuaPay, an early open banking leader may be for sale. Its parent company, Senteniel, was acquired by EML, the accident prone Australian fintech for €70m in 2021. Account to account payments are meant to be hard to spoof but Senteniel was then hit by A$8.5m merchant fraud in August 2022. Now the Irish regulator has raised anti-money laundering concerns and asset sales look likely.

Munich-based Ivyhas raised €7m for “instant bank payments your customers love.” It sits on top of Tink, TrueLayer or Token.io and looks like a very well thought-through proposition. Merchants need vendors to build compelling customer experiences on top of the raw capabilities provided by the API aggregators so this could be a winner.

Crypto corner

PayPal is hoping to legitimise crypto with its newly minted Paypal dollars but opinion is divided. Bank of America thinks PayPal is unlikely to win significant crypto market share but I suspect its analysts are missing the point. PayPal will focus on customer experience, global deployment, and ease of use in a sector notorious for operational complexity. If PayPal can’t make this work, nobody can.

Meanwhile, the regulatory clampdown on unbacked crypto is bringing results. Sex workers are complaining that crypto exchanges have been terminating their accountsciting reputational risk. One adult star left with a pile of unsaleable crypto tokens said “the whole ‘crypto is permissionless and censorship-resistant’ thing is a bunch of bullshit.”

No criminal could possibly need the new “No KYC Visa card” available to anyone with an Ethereum wallet. Jason Mikula explains that this wholly noncompliant boondoggle is most likely built on banking-as-a-service capabilities from Stripe.

Other news

Edgar Dunn writes on payment orchestration platforms (POPs). The consulting company counts 27 multi-acquirer platforms available today plus eight acquirers marketing their eCommerce gateways as orchestration platforms. The sector has attracted over $650m investment in recent years.

Poland is a fintech hotbed. There are over 80 payment businesses referenced in the 2023 Map of Polish Fintech.

If you want to become a wealthy payments sales person, here’s a handy guide from the US Electronic Transaction Association. Because independent sales agents are rewarded with small but long-lasting commission payments, the best advice is to be patient and love your customers.

The British Government has launched (yet another) Future of Payments Reviewalthough without clearly stating the problem it is trying to solve. No matter. The UK Payment Association has a handy survey for you to give your views.

The collapse of Railsr has caused havoc at Irish shopping centres, many of whom had sold open-loop gift cards issued by UAB Payrnet, a Ralisr subsidiary whose licence was revoked by the Lithuanian regulator.

Latest Wirecard news. Two ex-employees have been jailed in Singapore, the first criminal convictions anywhere in the world relating to the scandal. Meanwhile, Jan Marsalek, the fugitive COO, has claimed that Wirecard’s third party operations, whose existence or lack of existence, brought down the company, have continued to trade.

And finally

Worldline kindly invited me to join its Navigating Digital Payments podcast. If you’ve enjoyed this newsletter, give it a listen. Although I was certainly flattered to be asked to participate, my head isn’t normally this large.

Santander’s payment subsidiary, PagoNxt, posted another quarter of good results, with strong growth in payment volumes across all its major markets. This performance highlights the success of Santander’s strategy to in-source and consolidate its payment activities. PagoNxt comprises all of Santander’s payment assets, including Getnet, a leading multi-national merchant acquirer, Ebury (trade finance), Payments Hub, and Superdigital, a financial marketplace for the economic inclusion of the underbanked.

Getnet, PagoNxt’s merchant services unit grew total volume processed 22% in Q2 2023 to €49bn with ATV falling 9% to €21.78.

Volume grew in most major markets in the first half, with increases of 32% in Europe, 31% in Mexico and 15% in Brazil. The positive performance in Europe was driven by continued rebound in Spain as travel and tourism recover from the pandemic. The business opened Getnet Portugal with a range of Newland terminals nicely branded with Santander’s shade of red. It’s suprising how often banks miss the opportunity to use payment devices to raise brand awareness,

A core plank of the Getnet strategy is to expand the geographic footprint based on a standard set of global products. Management highlighted launches in H1 of a working capital solution, dynamic currency conversion, Android POS and vertical propositions for airlines and restaurants. The Android POS is called Get Smart and is available in Spain but only for customers with “a high volume of sales.”

In Latin America, where Getnet claims to be the third largest acquirer, the business has launched its services in Argentina and begun leveraging the global platforms in Mexico. Management expects to launch in Chile during the second half of this year.

Away from Getnet, PagoNxt says Payments Hub has made significant progress to become Santander’s wholesale payments processing provider. It claims that a “significant volume” of payments in Spain has already been migrated making the business “one of the largest A2A payment processors in the Eurozone.” Management also reports “making progress” in consolidating wholesale payments from operations in Brazil, Mexico and the UK to the Payments Hub global platform.

Total PagoNxt revenue from all divisions was up 17% at €277m in Q2 and with operating expenses rising just 14%, there was a slight improvement in the operating loss to €18m. The higher expenses reflect the “ongoing investment plans to develop and implement global technology.”

Santander’s payment arm, PagoNxt, reported a very positive start to 2023 with Q1 revenues surging 50% to €243m.

The division comprises several payment related units including Ebury for trade finance, Payments Hub for wholesale account-to-account payments and merchant services provider Getnet, which is of particular interest to Business of Payments.

Overall operating expenses at PagoNxt grew 46% to €278m resulting in an operating loss of €34m, slightly wider than the deficit of €28m recorded in the same quarter of 2022.

Getnet payment volume rose 34% to €45.6bn. Total transactions grew 32% to 2.132bn exceeding managements’ long-term target of 15% compound annual growth. Getnet’s average transaction value was €21.39.

Getnet’s operations closely follow Santander’s global footprint, with a focus on Latin America and Iberia. The company experienced a significant increase in volume in Mexico, with a 39% rise as it completed the migration of customers from Elavon, Santander’s former partner. In other Latin American countries, Getnet has launched in Argentina with Santander and reports further progress in Uruguay and Chile, where it will face competition from Global Payments, which inherited a local bank partnership after its acquisition of EVO Payments.

In Europe, Getnet’s volume grew by 35%, driven by strong performances in Spain and Portugal, where it recently launched a new set of propositions with Santander. These include an Android terminal with local value add services. Management says that it will complement the in-house bank distribution channel with direct sales.

Unlike some competitors, notably Sabadell, Santander’s management has reiterated its commitment to managing merchant payments in-house. At the recent Capital Markets Day, Santander revealed the killer statistic that banking customers that also take POS acquiring generate between 1.6 and 2.9 times the margin of those that do not. This underlines the strong synergy between payments and business banking.

Payments is one of a set of strategic “network” business lines which the bank believes diversifies its risk away from lending.

Payments – merchant services, cards and A2H – accounts for c.10% of group revenue today and will grow to 13% by 2025.

Santander showed one killer statistic that substantiates the economic rationale for SMB acquiring. In Spain, Santander banking customers that also take POS acquiring generate 2.1x the margin of those that don’t. The multiplier is 1.6 in Mexico and 2.9 in Brazil.

Global transaction volume is expected to rise and cost per transaction processed expected to fall. This virtuous circle results in significant projected profit increases.

Total payments transactions processed are forecast to grow 15% CAGR 2022-25. Growth is a little faster in Europe (+12%) than Latin America (+8%). Platform cost per transaction is projected to fall c.20% each year.

Within Santander’s payments portfolio, PagoNxt, the merchant facing division, should exceed 30% EBITDA margin by 2025 as volume grows and unit costs decline. On 2022 revenues of €953m this implies achievable EBITDA for PagoNxt of well over €300m, given current growth rates. If realised, this would show that Santander has created substantial value with the establishment of PagoNxt.

Santander’s payment subsidiary, PagoNxt, posted impressive results for Q4 2022, showing continued growth in payment volumes and achieving its first operating profit. This performance highlights the success of Santander’s strategy to in-source and consolidate its worldwide payment activities. PagoNxt comprises all of Santander’s payment assets, including Getnet, a leading multi-national merchant acquirer, Ebury (trade finance), Payments Hub (wholesale payments), and Superdigital, a financial marketplace for the economic inclusion of the underbanked.

Getnet, the largest division of PagoNxt, experienced substantial growth in Q4 with a 38% increase in payment volume to €48 billion, and a 42% increase for 2022 as a whole to €165 billion. The number of active merchants also increased 4% to 1.32 million, with an annualized payment volume per merchant rising 25% to €145,000.

Getnet has become the third-largest acquirer in Latin America, having launched acquiring businesses in Argentina and Uruguay and accelerating its presence in Chile. In Brazil, Getnet’s volume rose 16%, driven by strong eCommerce activity, while in Mexico, volume grew 35% due to increased average ticket size and new partnerships with financial institutions and ISVs. Anna Botin, Santander’s Chair, is particularly pleased with progress in Mexico explaining that merchant acquiring “is a key product to engage our customers and be able to do more business in the bank. We are currently #2 by total payment volume.”

In Europe, Getnet has expanded to include active customers in 12 countries, with strong growth driven by a booming Spanish market and the return of tourists. The company’s management reports it has developed a vertical solution for airlines. Europe volume grew 39%, also boosted by the transfer of Santander Portugal’s acquiring business to Getnet Europe.

PagoNxt’s overall financial performance was highly positive, with revenue growing 86% in Q4 to €298 million and expenses increasing 52%. Although the business only made a small operating profit of €3 million, this marks the first time it has been in the black, and is a positive sign for the future.