Global Payments’ Q1 results highlighted the remarkable impact of the Worldpay acquisition on the scale of its European business. The addition of Worldpay takes GP’s EMEA business to around €600m of quarterly net revenue – four times the level of three years ago. GP was generating just €150m per quarter in 2023. This roughly doubled following the EVO acquisition and has now doubled again. Global Payments’ European business is now larger than Nexi’s and only slightly smaller than Worldline’s.

The enlarged GP is now the largest acquirer in the UK (Worldpay’s heartland) and Poland (through eService, the JV with PKO BP inherited from EVO). It also has strong positions in Spain, Ireland and the Czech Republic, plus a toehold in Germany through its new JV with Commerzbank.

Integration between GP and Worldpay is well underway. The top four layers of the new organisation have now been defined, and the structure is explicitly global, with multinational teams organised around customer segments — SME (or SMB in American English), enterprise and platforms. Management says it remains on track to deliver $200m of additional sales and $600m of expense savings.

Genius, the POS software proposition, is central to GP’s SME strategy. Management believes that most small businesses will ultimately buy bundled payments and software, whether from GP or another provider. In the UK, the former Worldpay sales team, which previously lacked a POS software offering, is now selling Genius. Management sounded notably bullish:

“In the U.K. and Ireland, we are expanding the size of our successful mid-market and small corporate sales teams … early adoption has been encouraging, surpassing 500 locations in less than 60 days.”

Elsewhere:

“We continue to scale Genius across multiple markets such as Germany and Austria, with additional international launches planned later this year and next.”

In enterprise, there was a notable processing win at Morrisons, the large UK grocery chain, which has ended a long-standing relationship with Barclaycard. Transactions are already flowing and “we expect to have their full migration live this quarter.” GP has also won Aldi Süd’s processing business in both North America and Europe.

Other European wins announced included:

Decathlon — Spain

Lidl — Spain

ELZAB ECOPOWER, an electric vehicle charging station provider — Poland

DG Park, a car park app provider — Poland

Tescoma, a homeware retailer — Czechia

Sklavenitis, grocery — Greece

Finally, GP was also bullish about its indirect business in Europe:

“We recently expanded integrated and platforms into the U.K., where early results are exceeding expectations. Partner signings are nearly double our planned performance and feedback continues to validate a strong product-market fit.”

Worldline’s management responded to last month’s fraud allegations concerning its German business by commissioning two independent reviews. One will assess the remaining high-risk portfolio “to confirm its clean-up,” while the other, led by Oliver Wyman, will deliver a “comprehensive assessment” of Worldline’s compliance and risk framework. Initial findings are expected within weeks.

Despite a plunging share price and market cap now under €1bn, analysts aren’t calling Worldline a buy. The bonds are trading at less than 90 cents to the dollar. Rebuilding investor trust will require time, stable results and no more nasty surprises.

GTCR might want to hold off booking that profit just yet.

JP Morgan paid $800m for 48.5% of Greek fintech Viva Wallet in 2022 and announced a 50-person “payments innovation lab” in Athens. But the deal quickly soured and is now tied up in litigation in both Athens and London. In the latest twist, both sides are claiming victory. Despite the uncertainty, Viva seems to be doing well in the marketplace and has started calling itself the First Fintech Bank in Europe.

Figure 1 Photo credit Viva.com

Viva is part of a fast-growing group of well-funded, POS-focused European payment start-ups including SumUp, Flatpay, myPOS World and Dojo – some acquirers, some payment facilitators (PF). Let’s call them the Tap Pack.

SumUp, the Anglo-German PF that reported €1bn revenue and a maiden operating profit in 2024, has postponed its IPO to 2026. Valued at €8bn in its last funding round, analysts doubt that figure will hold in today’s market.

SumUp has also agreed, at long last to support Girocard payments. The move responds to two issues: Mastercard’s phase out of Maestro, and the German savings banks’ launch of S-Cube, a SumUp rival with Girocard bundled in.

Flatpay says it will sign 5,000 new merchants this month, boosted by its French expansion which claims 40 staff and 1,000 merchants already. Pricing is very keen – a free PAX A920 and all transactions at just 1.29%. The Danish PF is entering the UK next with the radical innovation of recruiting an in-house sales team in place of the usual network of self-employed agents.

The Tap Pack have been gaining ground at the expense of incumbents like Worldline and Barclaycard. But they now face pressure from a new wave of capital-light, unregulated startups offering a slick user experience on Adyen’s rails. Examples include Yetipay, Kody, and MyPOS Connect (not to be confused with MyPOS World).

London-based Yetipay just raised £3.5m in debt and equity for its hospitality payments platform. It claims to process £500m annually and generate £5m in revenue. The Adyen integration has enabled fast expansion into Spain and Italy. Here’s a photo of founder Oliver Pugh with what the press release questionably describes as a pink yeti.

Turning to SoftPOS, Rubean, listed on the Munich Stock Exchange, is finally seeing real growth. First-half 2025 revenues jumped to €2.54m, up from €0.84m a year earlier. Analysts expect full-year sales to double, and the stock has surged 35% to an all-time high of €8.75.

Rubean’s key selling points include Girocard support and integration with Redsys in Spain. Deichmann, the German shoe retailer, uses Rubean’s technology on Zebra handhelds into payment terminals. It’s a great example how SoftPOS can be transformational for enterprise retail.

In fundraising news:

Modern World Business Solutions (UK) raised £9m to scale from 60 to 200 staff. MWBS offers a white-label ISO-as-a-service platform and a comparison tool for SMEs seeking better payment deals.

Ontik, a London-based startup automating cash collection for the building trades, raised $3.7m. Payments are processed via Stripe or Yapily for open banking.

Paddle, the merchant-of-record platform for SaaS vendors, shrugged off a recent $5m US regulatory fine with a $25m debt raise. Its 2023 accounts showed a £46m operating loss on £57m revenue.Germany’s savings banks remain rare incumbent winners. S-Payment, their merchant services arm, grew revenue 13% to €292m in 2024, with mobile payments (Apple/Google Pay at POS) especially strong. Girocard transactions rose 12%, double the national average. And no red flags were raised in PayOne, the group’s JV with Worldline—which will reassure its beleaguered shareholders.

Scheming

Visa and Mastercard are facing mounting legal pressure in Europe. In a landmark UK ruling, a court found that commercial and inter-regional interchange fees breach competition law. Crucially, the court ruled interchange is anti-competitive “by object” – a first which could trigger a wave of merchant damages claims. Both networks plan to appeal.

Visa and Mastercard justify their fees by highlighting innovations such as tokenisation, now covering nearly half of Mastercard’s European transactions and Click to Pay, their long-delayed answer to PayPal. This is finally getting some serious marketing dollars although these don’t seem to have reached Poland.

With European payment sovereignty high on the political agenda, much depends on wero, the wallet backed by the European Payments Initiative (EPI). According to Finanz-Szene, EPI has raised an impressive €450m from shareholders including Worldline and Nexi. To succeed wero needs wide distribution through mobile banking apps and broad acceptance from merchants.

The distribution side is going well with five new Belgian banks added and Austria reportedly in talks. Wero claims 42 million users across Belgium, France, and Germany and processed €5bn in P2P volume in its first three months. eCommerce support is due this year, with in-store payments in 2026.

Wero hopes to link with Europe’s domestic mobile wallets, including Blik (Poland), Bancomat (Italy), Bizum (Spain), Vipps (Norway), IRIS (Greece), and MB Way (Portugal). Greece’s IRIS is likely to gain momentum thanks to a new law mandating acceptance both online and in-store.

The convergence of software and payments, pioneered in the USA, is now accelerating across Europe. A new report from Flagship Consulting highlights the extent to which PSPs are acquiring European software firms to gain distribution in key verticals like restaurants and retail. Let me know if you spot any they’ve missed.

American software vendors realised years ago they could double their margins by integrating payments. As Jim Roddy from the Retail Solution Providers Association puts it: “ISVs are the new ISOs.“I visited an RSPA member once, and the CEO didn’t show me new software. He shut the door, plugged in a TV, and pulled up a spreadsheet showing how much he made monthly from payments. The numbers were huge.”

Not all customers are thrilled. American restaurateurs are increasingly frustrated at being locked into inflexible, expensive payment setups bundled with their POS software. While competition authorities haven’t stepped in yet, scrutiny may not be far off, especially if merchants are barred from choosing their processor.

Acquirers hoping to partner with ISVs need to fully embed their offer within the software vendor’s customer proposition. That means API-based onboarding, access to management info, smooth customer service, transparent pricing, and generous commissions for the software partner.

Where does it go wrong? A Dutch restaurant shared on LinkedIn its experience of switching from Worldline to Viva. Integrating Viva’s terminals with its Odoo ECR software took less than two minutes. Worldline supports Odoo too but only via a special IoT box costing €35/month. The restaurant chose Viva despite higher transaction fees, citing better support and a simpler setup.

ChatGPT’s prototype shopping agent is slow and error-prone today, but it’s easy to see how it could soon become ubiquitous and render traditional eCommerce websites obsolete. If the AI already knows your shipping and payment info, what’s the point of a checkout page? Simon Taylor explores the implications. Startups like Ogment are already offering tools for merchants to adopt.

Shopify, the world’s leading eCommerce platform, is pushing back, posting a robots.txt file that directs agent developers to its official checkout SDK. Amazon is doing the same. As this LinkedIn discussion shows, Shopify’s move may upset tech purists but will please merchants already overwhelmed by bot traffic.

It’s still early days, and AI can’t yet be trusted. In one test, an AI managing an office vending machine lost money by over-discounting snacks and inexplicably stocking unsellable metal cubes.

Despite Amazon’s recent U-turn, checkout-free tech is gaining traction in high-traffic locations like stadiums. In Europe, we’re seeing rollouts in small grocery formats. Coca-Cola HBC plans 15 checkout-free stores in Hungary using low-cost Chinese AI from Cloudpick, integrated by Kende Retail and with payments by myPOS. This price is said to be just €40,000 for each shop.

Old fashioned vending is also rising as a payments channel. This 72-lane Boxbar drink dispenser in Manchester uses Adyen, Global Payments, and Viva for processing.

Having failed to commercialise virtual reality, Meta is now focusing on augmented reality via glasses and recently acquired a 3% stake in EssilorLuxottica, makers of Ray-Ban. It looks less ridiculous than a VR headset and you can imagine the power of AI seeing what you’re seeing and whispering helpful advice in your ear. Or maybe not. Matt Jones explains what it means for payments.

In Hong Kong, Alipay has launched smart glasses that let users pay by looking at a QR code and speaking the amount out loud. Rokid powers the app. Meizu has a similar product, with a dash of dystopia. People using these glasses don’t make eye contact and it’s very disconcerting as you can see from the video.

Product

Here’s a novel but quite risky idea. Better, based in Tel Aviv, is offering to step in to honour transactions where the card is declined due to insufficient funds. This start-up will “save the sale” by settling the merchant (less 10-15% commission) and waiting until after pay-day to put the transaction through. Better says it has already run a proof of concept with PayU. Similar products are available including Bounce.

Many subscription payment providers are struggling to keep up with the move by software vendors away from per seat or tiered pricing to models focused on how much data you crunch. Stripe reports that this “usage-based” billing is up 145% year to date.

Payments and loyalty

Rewe, the German supermarket giant with 3,800 stores, has launched Rewe Pay, a QR code wallet built by its in-house processor, Paymenttools. Setup is a bit clunky: shoppers register their Girocard, then complete a SEPA direct debit mandate via the app and sign their name on an in-store tablet. After that, payments are easy, made by scanning a QR code at checkout.

Commentators see Rewe Pay as a response to rising processing costs, especially as shoppers increasingly use Apple Pay linked to Visa and Mastercard, but the automatic incorporation of Rewe Bonus points on all purchases is equally interesting.

In a controlled, single-merchant environment like Rewe, the model should work. But I’ve long been sceptical of open-loop, card-linked loyalty. That idea has been around for years but has stumbled on technical barriers, unreliable merchant category code (MCC) data, and the difficulty of building profitable loyalty economics. Plus, card-linking offers benefits after the transaction, not before, making it hard for merchants to recognise high-value customers at the point of sale.

Paylead, based in Bordeaux, takes a bank-centric model, linking consumer ccounts to retail deals at the largest merchants such as Auchan and Decathlon. Paylead raised $6m in 2020. And Loyyo (Netherlands) replaces stamp cards with payment-linked rewards, is available via Adyen and CCV also recently secured new funding.

Fraud update

Chargebacks continue to rise. Ethoca projects global dispute volumes will hit 324 million by 2028, driven mainly by post-sale issues like slow refunds, unclear billing, and delivery friction, rather than outright fraud. The real pain is operational which has pushed merchants to look beyond traditional fraud tools. Visa’s Rapid Dispute Resolution (RDR) is gaining traction and is claimed to cut chargebacks by 20–30% for participating merchants.

So much for the carrot, here’s the stick. Visa’s updated Acquirer Monitoring Program(VAMP) is raising the stakes. Acquirers now face stricter thresholds, tighter enforcement, and the risk of fines, or even losing their membership if chargeback rates across their merchant portfolios climb too high. TrustPay (not to be confused with Trust Payments) has a solid explainer on the changes.

VAMP and Mastercard’s counterpart, the Excessive Fraud Merchant (EFM) programme, put pressure on acquirers and PSPs to take a more proactive role in policing their portfolios. In recent weeks, both Worldline and Paddle have shown the consequences of inattention. But for merchants, the message is equally clear: chargebacks are no longer just a cost of doing business, they’re a serious reputational and commercial risk that could jeopardise access to processing altogether

Car Commerce

The global auto industry is scrambling for new revenue and wants to pivot to a service-led model where drivers pay for parking, charging, or fuel directly through the vehicle’s OS. Naturally, the car brands want a cut. That’s why many are now resisting Apple’s “CarPlay Ultra”, which sidelines in-car payment systems. The problem? Motorists prefer to dock their phones and control everything from there. Top Gear takes a detailed look in this video.

Under pressure from government, the UK industry has agreed to roll out a National Parking Platformwhich allows any participating app to work across all publicly owned car parks. It’s already live at 476 locations, handling 550,000 transactions a month. There’s not that much money in parking payments. I calculate the three leaders in the UK market – Ringo, JustPark and Paybyphone – generate annual sales of c.£60m between them.

Open banking

UK open banking payments have stalled, with volumes flat at around 28 million transactions per month since early 2025. This reinforces the urgent need for a proper open banking scheme—with an acceptance mark, rulebook, consumer protection, and a business model that gives banks a reason to maintain high-quality APIs.

TrueLayer underscored the slow pace of adoption across Europe with new figures from France and Germany Despite claiming a 60% market share in France, it processes just €2bn annually; in Germany, it holds 30% with €1.4bn in volume. Nobody is getting rich soon. A new Stripe partnership may help, but patchy bank APIs continue to limit growth.

Meanwhile, Trustly appears to be the only open banking player making real money. In 2024, volumes rose 54% to $85bn, and net revenue grew 32% to $239m. “Adjusted”EBITDA was up 50% to $73m. Business remains strong in North America and Europe, where Trustly retained its UK Government tax contract. Note: these results come from a press release, not audited accounts.

Trustly’s profit engine is widely believed to be US gaming, so others are following. London-based Yaspa, which offers open banking payments with integrated KYC, has raised $12m to target US iGaming, through a new office in Atlanta.

In a completely different vertical, Bumper, a UK car finance company, has acquired Cocoon, an open banking payment vendor which says its product is used by 20% of car dealers.

Stable coins

There’s been an explosion of commentary on stablecoins following the approval of Trump’s Genius Act, which for the first time sets out a regulatory framework. Jason Mikula has the details. Genius has triggered a rush among banks, fintechs and retailers to launch their own digital dollars which will be backed 1:1 by US Treasuries, although, unlike dollars in a bank account, there is no deposit insurance.

Why would businesses want in? For one, they keep the interest on Treasury bonds. And for retailers, stablecoin wallets could cut card fees if shoppers preload value. But it’s unclear why everyday users, especially in European democracies with easy access to banking services, would hold a private currency with no consumer protection. “Unless you’re a criminal, there’s no use case,” says Ryan Cummings, former White House advisor.

Business of Payments readers likely have two questions:

When will stablecoins be used for retail payments?

As for profitability: probably not. If stablecoins are fungible, meaning a “Walmart dollar” is interchangeable with a “JPMorgan dollar” then margins may collapse to 10bps, in line with money market funds. Coinbase is already offering 4.1% on USDC, and as Andrew Dresdner notes, that leaves little room for profit.

In other news

The latest UK government payments strategy includes the formation of several new committees: a Payments Vision Delivery Committee, a Vision Engagement Group, and a Retail Payments Infrastructure Board. Undoubtedly good news for those who make a living sitting on industry panels.

In Denmark, NETS went down on Saturday 19 July, leaving Danes unable to use ATMs or POS terminals at home and abroad across Dankort, Visa, and Mastercard. One group of Danes stranded in Cyprus wrote: “Our plan for now is to try a live performance that includes both singing and dancing, but we are crossing our fingers that the problem is resolved before they refuse to serve us any more beers.”

Figure 2: Danes struggling to come to terms with the NETS outage

GTCR, which has little previous apparent interest in fintech, bought 55% of Worldpay for $13bn in cash and has committed a further $1.3bn for “strategic acquisitions.” These will likely focus on closing Worldpay’s product gap with Adyen and Stripe through extra capability related to servicing platforms/ISVs and on expanding Worldpay’s international POS capability to serve global, omnichannel retailers.

I asked Bing’s image creator to comment on the news. Surprisingly, Worldpay haven’t yet been in touch for the image rights.

Barclays, owner of Barclaycard, the UK’s second largest acquirer, has turned to private equity to rescue its underperforming payment division after having failed to find a trade buyer. Worldline, Nexi or Global Payments aren’t interested but Barclays is reportedly still looking for £2bn at 6.5x EBITDA.

The French do things differently. One week after Worldline appointed bankers to help avoid a possible hostile takeover triggered by its collapsing share price, Credit Agricole appeared as a white knight, taking a 7% stake. Worldline and Credit Agricole recently announced a JV and the French bank has a strong interest in ensuring Worldline goes through with the deal.

In Italy, Nexi is vying with Worldline for the merchant business of Cassa Centrale Banca, a group of 66 regional co-operative banks. CCB processes €2.2bn annual volume from 25,000 POS terminals and is looking for a valuation of €70-€100m. BCCPay, which recently scooped Nexi for a partnership with Banco BPM, and Market Pay, an aggressive new acquirer spun out of Carrefour, are also believed to be in the running.

Turning to Germany, Global Payments is forming a JV with Commerzbank. The new business, snappily called Commerz Globalpay, is 51% owned by Global Payments and will sell products to the bank’s large domestic corporate and SME customer base. While Commerzbank could be a great distribution channel, German banks are notoriously bad at lead generation. Fiserv launched a similar venture last year with Deutsche Bank which is reportedly underperforming.

There seems little prospect of many payment companies floating on public markets this year. According to one VC, many still haven’t adapted to today’s business conditions: “Where you have massive… processing volumes, but you’re still making negative margins, [this] is no longer acceptable.”

Stripe is also an IPO candidate for 2024 and rumoured to be preparing for floatation by raising prices and being much more discriminating about which customers it is prepared to onboard. One industry expert reports Stripe’s “out of the box API pricing” is 2x3x higher than a year ago. Higher prices and more cautious risk policies may trouble some of the fintechs and ISVs which have built their businesses on Stripe.

In case you missed these stories from from the Business of Payments blog:

Allpay, the UK public sector specialist, reported a very positive set of results. Few other payment companies can boast 21% revenue growth and 16% operating margins.

Trustly, one of the European leaders in A2A payments, reported a difficult 2022 as it recovered from a tricky situation with the Swedish regulator.

January trading updates had contrasting impacts on two London-listed payment companies with roots in carrier billing and names like childrens’ TV characters.

Boku, which is shifting its business towards global APMs competing with Thunes and dLocal, reported payment volume up 16% to $5.0bn and sales up 26% to $38m for H1 2023. Less happily, Bango, which has stayed closer to its original telco customer base, downgraded earnings expectations and lost 40% of its market capitalisation. Management says that new, value-added services are proving slow to deliver cash profits.

Checkout.com is the latest vendor to be designated a “significant provider” of card-acquiring services to SMEs in the UK and brought within scope of the Payment Systems Regulator’s directions. Checkout is normally associated with enterprise merchants, but its good performance is thought to be thanks to a growing PF relationship with Mollie, the Dutch PSP which has begun selling to UK small businesses.

Ant Group, the giant Chinese technology group behind Alibaba and Alipay, has made a smart move into European merchant payments with the proposed acquisition of MultiSafepay. This Amsterdam-based acquirer brings a modern omni-channel technology platform (with Sunmi POS terminals) and 18,000 SME customers but the $200m price tag is expensive. MultiSafepay made a net profit of just $1.4m on sales of $50m in 2022.

New shopping

Just walk out is the new self-checkout, concluded Primark’s Chief Architect after a visit to this year’s NRF Retail Show in New York. Although we’ve not seen much activity in the clothing sector, autonomous grocery and convenience openings are coming thick and fast.

Netto has opened what it claims to be Europe’s largest autonomous store in Regensburg, Germany. The technology is from Trigo and, at 800 sq metres with 5,000 SKUs, this is very impressive. Helpfully, fruit and vegetables are automatically weighed and added to the virtual basket when you take them off the shelves.

Trigo is also behind Aldi’s new SHOP&GO check-out free store in Greenwich, south London. There’s no need to download an app, just tap your payment card, or phone, at the entry gates.

You can get an idea of the potential of autonomous technology with this implementation at a UK football club which could eliminate the long queues inevitable when everyone wants to buy a drink at half-time. Sodexho, the catering company, runs the outlet. The technology is from AiFi.

Credit Agricole’s decision to launch a biometric payment card is equally unconvincing. The main advantage is not having to remember your PIN for transactions greater than €50, but this is what Apple Pay is for. Even the French bank’s supplier can see the writing on the wall. Zwipe is shuttering its biometric payment operation to focus resources on access control.

Despite every consumer carrying biometric ID in their personal phone, investors won’t give up on this. Polish fintech, Payvein,just announced fresh funding for its payment service based on Hitachi’s finger vein recognition technology.

What better way to give the thumbs down to biometrics than with AEVI’s suggestion of gesture based payments? The concept seems to involve waving at the payment device with a pre-registered hand signal. Presumably, not a rude one.

Cooking commerce may be a more fruitful concept. Kroger, the US retailer, has partnered with GE so you can buy groceries direct from the LCD screen on your oven. The new service was delivered via a software update to 150,000 domestic appliances.

Product

Apple, under pressure from the EU competition authorities, has finally opened up the iPhone’s NFC chip to 3rd party banking and wallet applications. The move may allow banks to bypass Apple Pay and its c.15bps charges. More excitingly for consumers, this service could facilitate a new market for open banking payments at POS. Mike Kelly explains how this might work. Excitement levels vary across Europe as Apple’s market share ranges from 55% in Denmark to just 10% in Poland. And the ruling excludes the UK. Because Brexit.

For years, PayPal had the best, friction-free online checkout in the business but this advantage has been eroded by Apple Pay, Stripe and others. These new checkouts also move fraud risk to the issuer which makes them more popular with merchants.

PayPal’s set of new product features should help claw back some of the lost ground, especially in Germany where it is still the number one eCommerce payment method. PayPal’s massive global base of 400m customer accounts and 25m merchants means its new one-click checkout recognises 70% of shoppers and is claimed to cut checkout time by more than half.

The product could help merchants benefit from faster checkout where Shopify recognises the customer although the fees will likely be higher than a standard payment gateway. Amazon tried something similar with Amazon Pay although this proposition has struggled and recently announced layoffs. Unlike Shopify, merchants view Amazon as a competitor and avoided offering Amazon Pay if they could.

Shopify is an absolute beast. Its head of engineering says he accepts 23,000 lines of code each weekday and the platform’s app servers handled 60m requests per minute on Black Friday. Blimey.

Irish customers will be delighted they can now use their Revolut card to buy a ticket on the Aer Lingus website. Revolut Pay, a new product, transforms what looks to the cardholder like a debit card transaction into an account transfer. Aer Lingus is reporting impressive performance. Cart abandonment rates are sub 10% and authorisation rates at 98.5% which is pretty good for the airline industry. Published merchant fees for Revolut Pay start at 1% + 20c.

Back in the real world, one obstacle to the growth of the circular economy is how to pay people for products sent for recycling. The Danish city of Aarhus has a solution with this reverse vending machine for disposable coffee cups. People get their deposits back by tapping their payment card. TOMRA provides the machinery and Shift4 the payment processing in this clever use of the Visa Direct and Mastercard Send products.

Computop, the German PSP part owned by Nexi, launched its “Pay to Drive”proposition for EV charging stations using the PAX IM 30 unattended terminals. Computop already has a good customer base in this sector including Compleo and Mercedes Pay for in-car payments.

In scheme news, Carte Bancaire has finally launched an account updater service with the unfortunate Franglais brand of Updat’R. Adyen, MONEXT and Lyra are the first PSP’s to offer the new product.

FX loading can often be a guilty secret in the payment industry. Many vendors depend on marking-up foreign currency transactions for a considerable proportion of their profits and can be vulnerable if their larger customers start to scrutinise their bills too closely. New research from FXC shows how the US providers charge extra fees to their international merchants.

Public policy is turning to how cash can be saved from extinction. The Swedish government has demanded proposals to safeguard access to cash despite the public’s clear preference for electronic money. Only 8% of Swedes used cash for their most recent purchase.

As people need less cash, the fixed costs of running ATM networks are spread over fewer transactions and many locations become uneconomic. In France, three big banks are pooling their ATMs and plan to reduce their number by 30%.

Financial inclusion is normally the reason cited for mandating cash acceptance but this argument ignores the huge benefits of bringing people into digital money. As this new report from the Atlanta Fed explains, people excluded from digital money are also excluded from much of the rest of the economy too. For a plain English description of financial exclusion, read this description of the business of cheque cashing in the US. A cash economy rips off the poor.

It’s still early days in the emerging SoftPOS market but Rubean looks like one of the European winners, having locked down a number of solid distribution partnerships and two enterprise customers in Spain. Read more on the Business of Payments blog.

MagicCube, based in California and one of the first wave of SoftPOS vendors has announced a go-to-market partnership with Shift4. The move comes two years after Shift4 invested in MagicCube and is likely to see the product come to Europe following the American acquirer’s merger with Finaro.

Bain, the consulting company, says that 2029 will be the year card transactions finally stop growing. But Dave Birch thinks we might be even closer to “peak card” than this, especially if large merchants integrate variable recurring payments (VRPs) into their apps. VRPs are the open banking substitute for both direct debits and card on file and promise a better customer experience for consumers at lower cost to merchants.

For the moment, open banking reality is some distance from this promise. A new study shows French banks rejecting 47% of payment transactions using their open banking APIs. “Is this the worst in Europe?” “ask the authors. “Far from it” reply the PSP’s. Portuguese banks are certainly worse. With standard bank API’s so difficult to use in many European markets, it’s no surprise that local schemes linked to SEPA Instant Payments such as iDEAL in Holland or Blik in Poland are prospering.

If the banks are to meet the challenge of producing better quality API’s they clearly need some help. Ozone API in London has raised £8.5m to commercialise its service that enables banks to offer open banking APIs.

The UK was first into open banking but, six years after the adoption of PSD2, the sector is having a long, dark night of the soul. As this good round-up demonstrates, there have been plenty of awards for open banking innovation but nobody is generating many transactions.

Ciaran O’Malley from Trustly posted a killer chart on LinkedIn which shows the extent of the commercial challenge for VRPs. In a two-sided market, there are few win-win scenarios.

This is why the Payment Systems Regulator (PSR) is proposing that the country’s largest banks will be mandated to offer VRPs at zero Interchange for government, utility and regulated financial services.

One of the many reasons Bitcoin has not replaced fiat money is that cryptocurrencies are horribly insecure, often run by crooks and with a terrible customer experience. As Dave Birch put it, “no sane person wants to be their own bank.”

The early hype around crypto set in train projects to launch central bank digital currencies (CBDCs). The Bank of England (BoE) received over 50,000 responses to its public consultation on the digital pound. Many of the concerns expressed were around privacy. The Bank promises that it won’t be able to see your individual transactions, but this won’t placate the zealots.

Any decision to launch Britcoin will be taken “around the middle of the decade” at the earliest but the BoE hasn’t answered the fundamental question of what a Central Bank Digital Currency (CBDC) is for. Neither does this video from the European Central Bank (ECB) shed much light on why anyone would want a digital euro rather than using Apple Pay.

The European Central Bank has begun tendering for some of the components of the digital euro. Worldline, Nexi and the EPI were involved in earlier prototyping exercises and will likely be bidding for the next set of contracts, valued at up to €1.1bn.

Research round-up

Cap Gemini’s payment trends for 2024 places real-time treasury and tokenisation in the top right quadrant. The consultants also see the card market growing in volume but losing share to A2A payments.

A summary up of 2024’s payment topics from the Finanz-Szene blog including wero, real-time bank transfers in Germany (at last) and the implication of TA 7.2 standards for payment terminals. A huge number of devices need replacing in Germany, notably the Verifone H5000s.

An Airwallex survey of SMBs highlights the embedded finance opportunities for payment providers. One interesting finding is that there is very little brand loyalty. 82% of merchants say they would change payment provider if their ISV offered a similar solution.

Chargeback 911’s annual Cardholder Dispute Index is always worth a read, if only to gasp at the average 5.7 disputes raised by each consumer every year in the USA.

35% of global eCommerce sales now go through marketplaces according to an absolute goldmine of omni-channel retail research available free of charge from RetailX. Retail CIOs themselves are planning major system upgrades to meet the needs of channel hopping consumers. This will likely trigger reassessments of their payment suppliers and is yet more bad news for incumbents saddled with legacy platforms.

In other news

UK retailers spent a whopping £1.27bn on card processing fees in 2023 and the British Retail Consortium is particularly annoyed about the 27% rise in scheme fees. The trade body is proposing that larger transactions should be charged as a fixed fee, not ad valorem; an idea likely to meet fierce resistance from the schemes.

One key application of AI is to automate customer service but you need to keep an eye on your robots otherwise they may start thinking for themselves. One AI chatbot working for DPD, a UK parcel delivery company with a mixed reputation, wrote a poem about how bad its employer was.

Where to find me

I’ll be moderating panel discussions at MPE in Berlin on 12-14 March and ePay Europe in London on 21 May. In between, you can catch me at Retail Expo in London on 24/25 April.

One of the key reasons for the collapse in Worldpay’s valuation is that when FIS bought the business, it was growing sales at about .9%. However, starved of funds under FIS’s ownership, Worldpay hasn’t been able to keep up with high-spending competitors such as Adyen, Stripe, Checkout and JP Morgan. The result: revenue was up just 1% in Q2, JP Morgan has overtaken Worldpay to the global number one spot and $25bn has disappeared.. More details on the Business of Payments blog.

In Europe, most attention is focused on battles for bank partnerships. In Italy, Banco BPM, advised by Bain Consulting, rejected its current partner, Nexi. Instead, in a surprise move, the Milan bank will merge its merchant services business with that of BCC Pay. The combined group, boasting 370,000 POS and €90bn volume, will claim number two spot in the Italian market and has the scale to compete with Nexi and Worldline.

Two other large European banks are in the process of finding partners for their merchant services arms. In France, Credit Agricole has now signed the agreement with Worldline to start a new JV. The revenue should start to flow in 2025. Again, there was less positive news for Nexi. The closure date for its acquisition of a majority stake in Sabadell’s merchant acquiring business (the second largest in Spain) has been put back six months to the first half of 2024.

Both Worldine and Nexi’s merchant services businesses themselves, seem in good underlying health. Reporting H1 results, Worldine revenue was up 13%. Management said it was still interested in acquiring merchant portfolios from banks. Nexi grew revenue 10% in H1 and is proving adept at realising synergies from the recent mergers with SIA, Nets and Concardis. It has decommissioned five of 25 processing platforms, says it’s on track to close another five in H2 and, longer term, to reduce the number to just four.

PagoNxt, Santander’s payment business, is also doing well. Volume was up 22% in Q2with increases recorded in all major markets in Europe and Latin America.

We’ve reported previously on the challenging market conditions for pure-play eCommerce gateways. It’s no surprise that privately owned Computop, which claims 30% of the German eCommerce market, has sold a 30% stake to Nexi. There is strategic logic for Nexi which already owns Concardis, Germany’s largest acquirer. Computop’s volume processed fell from €34bn in 2021 to €30bn in 2022. The decline is partly due the company’s decision to exit the gambling/adult sectors but also indicates competitive pressure from Adyen, Checkout and Stripe.

The decline in value of German payment assets was underlined by KKR’s decision to hand Unzer (formally HeidelPay) to its creditors, writing off most of its $668m investment. KKR acquired a majority stake in Heidelpay, a PSP with about 17% of the German eCommerce market, in 2019. Unzer was recently in trouble with BAFIN, the German financial regulator, due to “serious defects” in its risk processes.

US based Shift4 still hasn’t concluded its acquisition of Credorax Finaro, a European processor. First announced in March 2022, the deal hit regulatory obstacles linked to a sanctioned Russian oligarch on the Finaro share register. Management says it is confident of closing the deal in Q4.

Ryan Reynolds is a much better proposition as shareholder. After taking an undisclosed stake in Nuvei, a Canadian processor with global ambitions, the actor is fronting a witty and self-deprecating brand advertising campaign. Reynolds’ investment is already under water. Nuvei’s stock fell 39% after disappointing Q2 results.

Rapyd, the London based global “fintech as a service” provider, has paid $610m for the slowest growing and least profitable parts of the sprawling PayU empire. The purchase price will be financed by a fresh capital injection into Rapyd in what the company claims could be the largest Fintech fundraise of 2023. Arik Shtilman, CEO, took to LinkedIn to explain the rationale. “If you don’t aim for a big outcome, you won’t get an outsized return,” he says. More details on the Business of Payments blog.

We reported last month that Toast, a leading US restaurant software vendor with integral payment processing, had shocked its merchants by adding a $0.99c service charge to each bill. The fee would have been paid by diners and provide Toast with free money at 100% gross margin. The company has now back tracked with its CEO recognising “we made the wrong decision.”

Shift4, with time on its hands waiting for the Finaro deal to close, responded with a clever “Don’t get Toasted” campaign.

Synch Payments, an attempt by a consortium of Irish banks to produce a domestic mobile money transfer app to rival Revolut, has been delayed once more. Again, it’s Nexi supplying the technology.

While autonomous stores are gaining traction across Europe, Amazon, which invented the technology, is struggling. According to the RTHI blog, Amazon’s stores are in the wrong place, have the wrong products, cost too much to build and are confusing for customers. For example, you can now checkout by tapping your physical payment card but not with Apple/Google Pay. Or with Amex. The stores don’t even accept Amazon gift cards.

Customer satisfaction with traditional self-checkouts is falling. Shoppers resent the ongoing reduction in staffed checkout. With autonomous stores so expensive, smart carts may provide a cheaper and more flexible compromise. Here’s a good round up from Forbes on the state of play. Kroger, the US grocer, says smart cart shoppers spend less time in store but spend more money. Everyone’s a winner.

Shoppers are returning to local stores. As expected, once confronted with the true economic cost of rapid grocery deliveries, people are willing to walk to the shops just like it’s 2019. The last mile delivery specialists are disappearing one by one. Getir is the latest to urgently need more cash to keep trading. Maybe robot deliveries are the answer.

Fans of biometric payments will be delighted that Amazon is rolling out Amazon One, its palm payment product, to 500 US Wholefood stores by the end of this year. Amazon says the technology has been used 1m times to date with zero false positives and is ideal for high volume locations such as stadiums. Shoppers first need to visit an Amazon One location where they can scan their palm and link it with their Amazon account.

Palm payments are no more convenient for shoppers than Apple/Google Pay. But there is clear benefit to Amazon of capturing extra customer data and/or being able to steer transactions to lower cost payment methods.

While Amazon can probably be trusted to keep your data safe, other vendors may not be so reliable. For example Worldcoin, a San Francisco-based start-up, is creating a global identity database founded on iris scanning and secured $115m funding in May this year. Its focus has been mainly on developing countries such as Kenya, in which Worldcoin has been asking people to agree to having their eyeballs scanned in return for $50 in tokens on the blockchain. What could possibly go wrong? Bain Capital is one of the VCs which should know better than be mixed up in this madness.

Product

Legacy acquirer like Worldpay and Barclaycard need to make rapid product investments to keep up with the new capabilities showcased by Adyen, Checkout and Stripe.

Optimised checkout is a great example. This uses AI to configure checkout pages with the best selection of payment brands, ensures that transactions contain the correct data and optimises routing to maximise acceptance or minimise cost. Stripe claims merchants moving to its optimised checkout grew sales revenue 10.5% more than a control group which stayed on the old product. Checkout says its Intelligent Acceptance product increased acceptance rates by up to 9.5ppts. Early customers include Klarna.

Checkout.com has also launched Identity Verification which, it says, uses AI to identify individuals within 120 seconds as they video themselves holding up identity documents. Uber Eats is an early customer.

Adyen announced Data Connect for Marketing which helps merchants identify their in-store customers. Retailers used to this themselves before PCI regulations banned them from storing customers’ card details in their own systems. Impressively, Adyen is also the first Fintech to join FedNow, the new US instant interbank payment network.

Subscribed

Away from the global processors, Cashflows, a UK eCommerce acquirer, has added a range of Castles POS terminals as part of omni-channel proposition to its ISV and ISO distribution partners. This is a smart move. New UK regulation has outlawed lengthy POS terminal rental contracts but were connected to one of the 14 largest acquirers. Cashflows is not one of the 14 and so will be an attractive option for ISOs looking to continue business as usual.

Far Eastern tourists are back in Paris to shop and the top retailers know they need to offer their favourite ways to pay. Printemps, a leading department store, has integrated Alipay+ into its POS checkout flow. Alipay+ also gives access to Kakao Pay (South Korea), GCash (Philippines), Touch ‘n Go (Malaysia) and TrueMoney (Thailand).

Fuel cards are commonly issued to staff who drive company vehicles but there’s always a risk of fraud or misuse. A new idea from CarIQ uses vehicle data as a sort of biometric ID. Linked to a virtual card, the vehicle pays for its own fuel, without the driver needing to sign for the gas. CarlQ has just signed a global partnership with Visa.

Access to cash

As cash usage declines, a growing number of merchants are only accepting digital payment. This presents problems in societies where some citizens don’t have access to electronic money. But cash-free stores are also enraging many of the people already angry about vaccines, traffic restrictions, 5G masts and sundry other inevitable aspects of modern life.

If cash is to be preserved, public policy needs to address the fact that the less cash is used, the more expensive it gets. For example UK convenience stores often host ATM machines with the retailer receiving a commission of 15p per withdrawal. One store reports transactions down 70% at a “free” ATM. The result: the retailer is not making enough revenue and is switching to an ATM that charges customers a withdrawal fee. The likely outcome is that transactions will fall further.

SoftPOS has only been available on Android so news of the European launch of Apple’s “Tap to Pay” on iPhone made the headlines. Apple’s SoftPOS is based on the $100m acquisition of Montreal-based Mobeewave in 2020. Architected differently to Android SoftPOS, Apple offers an SDK to developers/PSPs allowing them to build payment acceptance capability into their own iPhone apps.

With Apple SoftPOS, there’s still a need for an acquirer (or payment facilitator) to process the transactions but no obvious role for the specialist payment app/gateway providers such as MyPinPad or Phos. Happily for the SoftPOS start-ups, the Android market is large enough to keep them all busy for some time.

In Android product news, Oona, a Finnish start-up, has some interesting enterprise SoftPOS ideas such as this kiosk, for which Rubean provided the payment application. Getnet (Santander) has launched SoftPOS in Spain although only for larger business customers. Finally, Worldine is now live with SoftPOS in Italy via its new Banco Desio partnership supported by a clever TV commercial.

Open banking

Natwest, which has modestly taken the URL www.bankofapis.com, commissioned a report to identify the key obstacles holding back the wider adoption of Open Banking. It concludes the problems lie in “lack of commercial incentives” to develop or enhance the core APIs and “lack of alignment between.. .banks.” Or as Nick Dunse, former CMO of Pay with Bolt wrote on LinkedIn, “Nobody is leading it and there’s no money in it.”

Some Fintech lobbyists are asking the regulator to lead by expanding the number of services available but Oliver Wyman, the management consultant, thinks its time for banks to introduce financial incentives for themselves by monetising the APIs. The consultants suggest that a typical bank could make $50-$75m per annum if it charged PSPs for value added services linked to the open banking APIs.

Variable recurring payments (VRP) – an open banking equivalent to direct debits – were meant kick start the sector in 2023 but have also been rather slow to take off. Here’s a good podcast from Edgar Dunn which explains how VRPs work and what the opportunities might be.

In corporate news, NuaPay, an early open banking leader may be for sale. Its parent company, Senteniel, was acquired by EML, the accident prone Australian fintech for €70m in 2021. Account to account payments are meant to be hard to spoof but Senteniel was then hit by A$8.5m merchant fraud in August 2022. Now the Irish regulator has raised anti-money laundering concerns and asset sales look likely.

Munich-based Ivyhas raised €7m for “instant bank payments your customers love.” It sits on top of Tink, TrueLayer or Token.io and looks like a very well thought-through proposition. Merchants need vendors to build compelling customer experiences on top of the raw capabilities provided by the API aggregators so this could be a winner.

Crypto corner

PayPal is hoping to legitimise crypto with its newly minted Paypal dollars but opinion is divided. Bank of America thinks PayPal is unlikely to win significant crypto market share but I suspect its analysts are missing the point. PayPal will focus on customer experience, global deployment, and ease of use in a sector notorious for operational complexity. If PayPal can’t make this work, nobody can.

Meanwhile, the regulatory clampdown on unbacked crypto is bringing results. Sex workers are complaining that crypto exchanges have been terminating their accountsciting reputational risk. One adult star left with a pile of unsaleable crypto tokens said “the whole ‘crypto is permissionless and censorship-resistant’ thing is a bunch of bullshit.”

No criminal could possibly need the new “No KYC Visa card” available to anyone with an Ethereum wallet. Jason Mikula explains that this wholly noncompliant boondoggle is most likely built on banking-as-a-service capabilities from Stripe.

Other news

Edgar Dunn writes on payment orchestration platforms (POPs). The consulting company counts 27 multi-acquirer platforms available today plus eight acquirers marketing their eCommerce gateways as orchestration platforms. The sector has attracted over $650m investment in recent years.

Poland is a fintech hotbed. There are over 80 payment businesses referenced in the 2023 Map of Polish Fintech.

If you want to become a wealthy payments sales person, here’s a handy guide from the US Electronic Transaction Association. Because independent sales agents are rewarded with small but long-lasting commission payments, the best advice is to be patient and love your customers.

The British Government has launched (yet another) Future of Payments Reviewalthough without clearly stating the problem it is trying to solve. No matter. The UK Payment Association has a handy survey for you to give your views.

The collapse of Railsr has caused havoc at Irish shopping centres, many of whom had sold open-loop gift cards issued by UAB Payrnet, a Ralisr subsidiary whose licence was revoked by the Lithuanian regulator.

Latest Wirecard news. Two ex-employees have been jailed in Singapore, the first criminal convictions anywhere in the world relating to the scandal. Meanwhile, Jan Marsalek, the fugitive COO, has claimed that Wirecard’s third party operations, whose existence or lack of existence, brought down the company, have continued to trade.

And finally

Worldline kindly invited me to join its Navigating Digital Payments podcast. If you’ve enjoyed this newsletter, give it a listen. Although I was certainly flattered to be asked to participate, my head isn’t normally this large.

Worldpay has lost its crown as the world’s number one merchant acquirer, although only by a very narrow margin. In each of the last four quarters, JP Morgan has processed a greater volume of payments.

Worldpay has been hobbled by having, in FIS, a cash-strapped parent unwilling or unable to invest. The challenges were spelled out earlier this year when FIS took an $18bn write down on its acquisition of Worldpay. We covered this in detail at the time. Now, Worldpay is to be spun-out of FIS as a joint-venture with GTCR, a Chicago private equity firm.

Meanwhile, Q2 results demonstrate the extent of Worldpay’s problems. Global payment volume grew 6% in Q2 to €591bn, once again lower than JPM which recorded an increase of 10% to $600bn. At Worldpay, another weak US performance (+4%) was offset by a healthier 11% increase in international volume but, over the last twelve months, JPM has processed $2287bn against $2266bn for Worldpay.

Underlining the reason for divesting its merchant solutions business, FIS reported Worldpay revenue rose just 1% in Q2 to $1.312bn “with similar sub-segment trends as seen in the first quarter”’ This likely means double digit growth in global eCommerce but continued revenue declines in the domestically focused US and UK businesses which are most badly in need of investment. Take rate fell 1bps to 22bps. ATV rose 2% to $46.17.

Worldpay adjusted EBITDA did rise but only by 3% to $634m. Margins expanded 120bps to 48.3% “as we grew our high-margin revenue streams across the operating segment and delivered on cost management.”

FIS management had first proposed a stock market flotation for Worldpay but now say that the partial trade sale is the best option as it can realise value faster and get a cash injection more quickly. It will sell 55% of Worldpay to GTCR, a private equity business with one successful payment investment under its belt. GTCR bought Sage Pay US in 2017 for $260m, floated it as Paya and sold it to Nuvei earlier this year for $1.3bn. Worldpay’s new valuation of $18.5bn is rather less than the $43bn FIS paid for the company in 2019. However, the price does represent 10x EBITDA, which is in excess of the 8x valuation of FIS as a whole prior to the announcement. To financial analysts, this represents value creation.

Looking ahead, management says that Worldpay “will remain an important partner and distribution channel for FIS” and that Worldpay will continue to benefit from access to FIS banking technology services and solutions. Backing from GTCR will “also ensure that Worldpay will have ample access to capital to pursue near-term inorganic growth opportunities.” Now is a good time to be shopping for payment capabilities. Valuations are lower than they have been for some time and we can expect Worldpay’s new owners to move fast to make up for its wilderness years with FIS.

Press reports and analyst comments indicate that PayU’s businesses outside of India and Turkey are for sale in a process being run by Bank of America. Worldpay, Rapyd, and Nuvei are said to vying to take control of the emerging market PSP. The target price is said to be $250m.

PayU is owned by Prosus, the Amsterdam-listed investment unit of South African Naspers, which hit the jackpot as an early investor in Tencent. Prosus has published its results for the year ending March 2023, shedding some light on PayU’s recent performance.

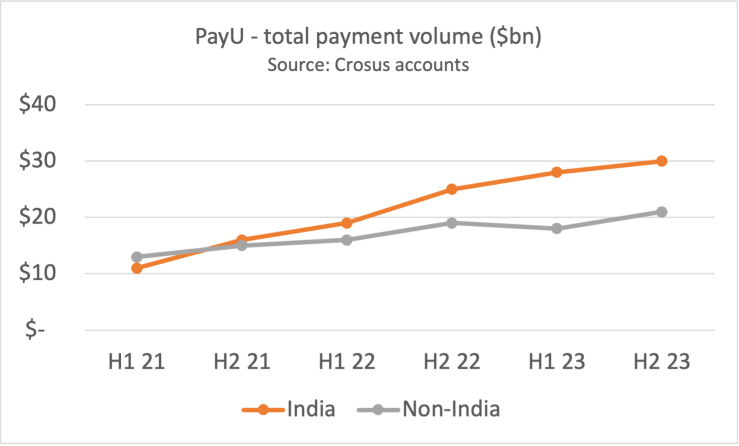

PayU’s payment volume grew 23% in FY 2023 to $97 billion. Most of the growth came from its 8m SME customers in India. Volume processed on the subcontinent rose 32% to $58 billion. What management describes as its Global Payments Organization (GPO), which includes all PayU business outside India, saw volumes rise just 11% to $39 billion.

Revenue from PayU’s core PSP business grew 23% to $792 million, driven by a strong performance in India and Turkey. Sales in India overtook the rest of the world for the first time, recording a turnover of $399 million, a rise of 31%. Outside India, revenue was up a more modest 15% at $393 million. Of this figure, roughly one third comes from Turkey (not included in the sale process) and another third from Poland (which is).

ATV was up 5% in India to $40.39 and remained flat outside India at $31.45.

The take rate in India was flat at 0.69% but rose 4 basis points in the rest of the world (RoW) to 1.01%. PayU provides eCommerce gateway services and payment orchestration but is not an acquirer, so a 1% take rate is reasonable. It represents an average revenue of 30 cents per transaction.

PayU recorded a trading profit of $11 million in India with a margin of 3%. Outside India, PayU lost $14 million, although it would have made a small profit except for a £23 million provision “related to merchants in Brazil and in the travel industry.”

PayU also booked $143 million in revenue and a trading loss of $27m on its 21% minority stake in Remitly.

Divesting the non-Indian and Turkish PayU businesses makes sense. These other markets are growing slowly and, collectively, are barely profitable. A trade buyer should be able to find plenty of synergies although the numerous technical platforms might be challenging to integrate. PayU also brings scale in Poland where it includes the former Allegro Payments, spun out of Europe’s leading online marketplace which was formerly owned by Naspers. PayU Poland recorded revenues of $248m in 2021. You can read more at Cashless.pl.

Of the three potential suitors, Rapyd has the strongest emerging market focus today and probably best understands this corner of the payment world. On the other hand, Worldpay badly needs a growth story to tell when it demerges from FIS in early 2024 and PayU might fit the bill. As for Nuvei, it has Ryan Reynolds on its share register so anything is possible.

Pay U has built its business largely through acquisition. Key purchases include:

Wibmo – Indian based white-label payment gateway bought by Pay U for $70m in 2019. Wibmo claims to have 160 bank and fintechs as customers in over 30 countries processing over 3bn transactions annually. Pay U laid off 150 staff in India at the end of 2022

Citrus Pay – a mobile wallet and gateway business operating in India, bought for for $130m in 2016. Citrus Pay claims $3bn processed annually.

Zooz – one of the first payment orchestrators, Israeli based Zooz was bought by Pay U in 2018, reportedly for between $80 and $100m. Zooz technology is at the heart of Pay U’s “payments hub” which connects its various technical capabilities.

Red Dot Payment – based in Singapore, Red Dot offers an webshop in a box, including payments, for micro merchants. Pay U acquired the business at a $65m valuation in 2019.

Iyzico – Pay U purchased this Turkish POS and eCommerce PSP with mobile focus for $165m in 2019. H&M, and Decathalon are customers. Iyzico processes 65bn lira annually which is around $2.5bn today at today’s exchange rates.

We’ll have to wait until FIS reports its Q1 numbers, but JP Morgan have likely just overtaken Worldpay to claim the prize as the world’s largest merchant acquirer. In the first quarter of 2023, merchant processing volume was up 14% at $559bn.

New management at FIS is moving quickly to repair the damage done by the company’s botched takeover of Worldpay in 2019. Stephanie Ferris, the incoming CEO, announced that Worldpay would be demerged this year with a separate listing on the stock market. She also booked an associated $17.7bn write down of the $43bn purchase.

Although the FIS board has been under pressure from activist investors, Ferris was Worldpay’s CFO prior to its acquisition by FIS and then worked as COO at FIS overseeing the merger integration. She probably came to her own realisation that Gary Norcross, her predecessor as CEO, had got the strategy badly wrong.

So, why is FIS demerging a business it only acquired three years ago? Well, the strategic rationale slide from the last week’s results deck won’t enlighten you much. I’m baffled investors put up with such flimsy written material.

The investor call itself supplied a little more detail. Stephanie Ferris said that capital allocation is driving the decision. Worldpay is stagnating and needs access to investment dollars to make the acquisitions it needs to keep up with Stripe, Adyen and JP Morgan. Ferris believes the current ownership, with its conservative balance sheet, cannot provide the capital needed to generate growth. She explained “specifically, the separation will enable FIS to target a strong investment grade credit rating, while allowing Worldpay to invest more aggressively for growth.”

Ferris was clear that Worldpay’s recent poor performance has been, in part, due to key product gaps and that FIS’s cautious capital structure had stymied its ability to buy-in or build capability. As an independent business, Worldpay will be able to raise the money it needs. In contrast, once free of its troublesome merchant acquirer, the rump FIS promises to be an investment grade stock paying steady dividends once more.

Shareholders did not welcome the move. Shares fell sharply on the news but no analyst on the investor call asked about the write down. Why $17.7bn? What went wrong? How is Fiserv, FIS’s arch-rival, seemingly make the exact same strategy work? FIS shares trade at less than half their value before Worldpay joined its family. Nobody apologised to shareholders for this value destruction.

It’s worth looking at why FIS bought Worldpay in the first place but before examining the deal rationale, let’s look at the history. Fifth Third Bank Corp span out its merchant processing division in 2009 with the help of Advent. This business was renamed Vantiv and bought London-based Worldpay for $10.4bn in 2017 bringing “together global scale, integrated technology, and diverse distribution to create a market leader in payment technology to power omni-commerce.”

Worldpay itself had been spun out of Royal Bank of Scotland with investment from Advent and Bain. Although Vantiv was the bigger partner and the HQ was to be in the US, the combined company chose to call itself Worldpay, which is a fine name for a payment brand. The combined business was valued at $28.8bn.

Less than two years later, FIS made its move and paid $43bn (including $8bn debt) for new Worldpay. As a rather staid provider of software and services to banks, FIS was feeling left out of the Fintech boom. Many commentators felt the Worldpay acquisition gave FIS a growth story. “The global payments industry is moving at an accelerated speed, and it is vital that large providers such as FIS stay ahead,” said Rivka Gewirtz Little of IDC Financial Insights.

The 2019 deal rationale was based mainly on revenue synergies from cross-selling merchant acquiring to FIS’s bank customers although management also believed that FIS products would be interesting to Worldpay’s merchants. The four main revenue drivers were expected to be:

Helping Worldpay to expand into emerging markets where FIS has a large footprint such as Brazil and India

Faster growth in eCommerce “through Worldpay’s expertise and ability to accept hundreds of payment types and currencies and FIS’ reach.”

Leveraging FIS’ leadership in the issuing market to offer loyalty programmes to Worldpay’s merchant customers

Using FIS’ expertise in open banking APIs to extend Worldpay’s acceptance offer beyond cards and wallets

None of these worked out. Cross-selling is always hard. Cross-selling anything to banks is even harder. Despite its heritage, Worldpay was never set up to partner with banks, the way that Global Payments, Worldline or First Data is organised. FIS didn’t pick up any new bank partnerships for Worldpay. In fact, it contrived to lose its main UK bank relationship when Natwest launched Tyl.

Integrating the two businesses, overseen by Stephanie Ferris in her role as FIS COO, took longer and was more expensive than hoped. Three years after the merger, the costs are still racking up. FIS charged $950m in 2022 “primarily to acquisition and integration costs primarily related to the Worldpay acquisition.”

Fast forward to 2022 and FIS management is now excited to say that the spin-off will create two market leaders – FIS as supplier of technology to banks and other financial institutions and Worldpay as the world’s largest global acquirer. At least for the moment. Worldpay’s FY 2022 volume was $2.2 trillion. JP Morgan, which grew 14% in 2022, is snapping at its heals and will likely be number one in 2023.

Management says the priorities for the newly independent Worldpay will be expanding in eCommerce (new geographies and “’payment optimisation”), strengthening its enterprise offerings including omni-channel and transforming SMB towards providing embedded finance working with ISVs. The latter is a recognition that its legacy ISO and direct SMB customers on both sides of the Atlantic are under sustained attack.

Charles Drucker, Worldpay’s CEO in 2019, returns to lead the business. He will need to quickly stabilise the poor financial performance which triggered the demerger. Although Worldpay was supposed to be the growth engine that transformed FIS’s fortunes, sales actually fell in Q4 2022, by 1% to $1.178b. Within Worldpay, a positive Q4 result from Global eCommerce, about 30% of revenue, was offset by continued sales declines in Enterprise (which includes the UK) and SMB. Erik Hoag, CFO, spelled out the problem: “These trends in SMB reflect a lack of new product investment, which we believe the [demerger] will best enable us to remedy. And in Enterprise, we saw economic weakness in the UK and anticipate further deterioration this year.”

Worldpay revenues are expected to decline a further 2%-4% in 2023 although I expect new management is assertively managing expectations. These numbers are likely to be very much a worst case scenario but it’s going to be hard for strong growth in Global eCommerce to overcome continued weakness in Enterprise (notably in the UK) and SMB.

FIS will soon be publishing more detail on Worldpay’s financial situation and market positions. It’s going to be fascinating to see how, as an independent business, it plans to invest to win in what is becoming a very competitive market.

Soon after Stripe’s announcement of mass layoffs, FIS used its Q3 results to warn investors that future revenue and profits would be lower than expected. Gary Norcross, in his last call before stepping up from CEO to Chairman, said “We are not pleased with the profitability performance of the business.”

Stefanie Ferris, the incoming CEO, will respond by taking $500m out of the company’s cost base in an “enterprise transformation” programme that will include job cuts, organisational restructuring and lower capital spending. Harris promised “the outsourcing of non-value-added activities and reviewing and rightsizing the current workforce.” Meanwhile, FIS booked a further $60m expense related to company’s never ending platform modernisation project.

Total revenue was up just 3% in Q3 at $3.6bn with low growth in all three divisions – capital markets, banking solutions and merchant solutions. Management said it was seeing “early signs of US consumer shifting spend from discretionary to non- discretionary verticals pressuring yield.”

Despite clear indications of inflationary pressures, especially in wages, “due to competitive job markets for the skilled employees who support our businesses,” FIS has costs under control. SG&A was down 1% at $977m.

Total adjusted EBITDA, the company’s preferred measure of profitability, was up 1% at $1.575bn. Net income was flattered by a $225m gain on the sale of its remaining stake in Capco Consulting to Wipro.

The merchant solutions division most interests us at Business of Payments. Merchant payment volume was up 3% to $544bn as weak performance in the UK was aggravated by the strong dollar. International volume was down 4% to $132bn. US volume was up 5% to $412bn, a little healthier but still lagging FIS’s competitors. FIS lost one large Payfac client which knocked 1ppt off global volume (c. $20bn annualised)

Merchant solutions revenue was up just 2% at $1.18bn. Management said growth would have been 6% excluding impacts of the Ukraine War and Sterling’s weakness.

Within Merchant Solutions, Global eCommerce continues to perform well, delivering 22% revenue growth at constant currencies, and signing new customers including Asian airline carriers. FIS is happy with the initial success of its guaranteed payment product in which merchants pay extra to have FIS cover any fraud losses. FIS continues to invest in Global eCommerce as “we expect e-commerce to ultimately account for 50% plus of total segment revenue.”

In contrast, FIS recognises systemic problems in SMB (revenues down 1%) and UK enterprise, the former Worldpay UK, which saw sales fall 15% at constant currencies. Both divisions are heavily dependent on POS payments at old economy merchants in “big box retail, grocery and pharmacy.”

These are non-discretionary consumer spend categories and should be recession resistant but FIS says its UK business is “continuing to see macro softness impacting revenue growth.” Ferris believes the UK is already in recession “and then they changed Prime Ministers at least once, maybe twice. And so the economic conditions in the UK are pretty challenging. And as we look out even over the next 60 days, it’s tough to call it. They are in a recession, their consumers are struggling, and we are tied to consumer spend.”

Recession or not, with consumer inflation at 10%, merchant acquiring revenues should not be falling 15%. The UK performance indicates FIS is losing significant market share.

SMB “has been adversely impacted by changing market dynamics,” said Harris. FIS is still selling POS acceptance through ISOs but merchant buying behaviour is moving to omni-channel payment solutions sourced from ISVs. Ferris, the new CEO, said “we’re strategically deprioritizing [SMB] and moving all of those partners that we’ve historically had there over to our embedded payment strategy with Worldpay for Platforms.” The latter is a new product based on the Payrix acquisition which allows Worldpay to compete with Adyen and Stripe for business with complex ISVs such as marketplaces.

Merchant solutions EBITDA was down 7% at $555m with margins falling 4ppt to 47% “primarily due to inflationary cost pressures and accelerated investment in e-commerce and Payrix sales channels to capitalize on developing secular growth trends.”

Banking solutions revenue was up 4% at $1.68bn in Q3. FIS blamed longer sales cycles for this lacklustre performance. The much smaller Capital Markets unit grew revenue 3% to $671m.

FIS reported moderate growth in its merchant solutions business in Q2 2022. Revenue was up 11% but margins contracted by 280bps. Woody Woodal, CFO, said “We continue to see wage inflation as an ongoing challenge” but he was relaxed about wider price increases as “we’ve been able to offset rising costs.”

Sales were boosted by a strong performance by the Global eCommerce division which was up 28%. Airline and travel clients have bounced back after the pandemic. The enterprise and SMB sectors saw revenue growth at under 10%.

Margins were hit by the impact of disinvestment in Russia (100bps), extra investment to support Global eCommerce and in beefing up domestic sales channels to support online merchants following the Payrix acquisition earlier this year.

Payrix is a payment-as-a-service offering that allows eCommerce ISVs to integrate payment processing with their software, either as a payment facilitator or simply white labelling the standard merchant acquiring offer. Payrix gives FIS access to a large and growing market segment but also the opportunity to upsell eCommerce payments to its in-store ISV partners.

Gary Norcross, CEO, is particularly excited about the new partnership with Signifyd which allows FIS to offer guaranteed payments to its merchant customers. Many online merchants are at significant risk from fraud and miss out on business by setting their parameters too strictly and rejecting good customers. With Worldpay Guaranteed Payments, FIS decides which customers are honest and shoulders the risk of fraud or chargebacks if the transaction goes bad. Merchants are assured that they will get paid and, says FIS, are prepared to pay handsomely for this. According to Norcross “we’re able to increase our revenue… doubling what we’re earning over processing revenue.”

FIS is a huge company which means some quite large numbers can be lost in the small print. Constructing the new HQ is not a cheap exercise with a total of $156m spent in the past twelve months. And FIS booked a further $160m “associated with the company’s platform modernisation.”