The payments business

Worldline’s management responded to last month’s fraud allegations concerning its German business by commissioning two independent reviews. One will assess the remaining high-risk portfolio “to confirm its clean-up,” while the other, led by Oliver Wyman, will deliver a “comprehensive assessment” of Worldline’s compliance and risk framework. Initial findings are expected within weeks.

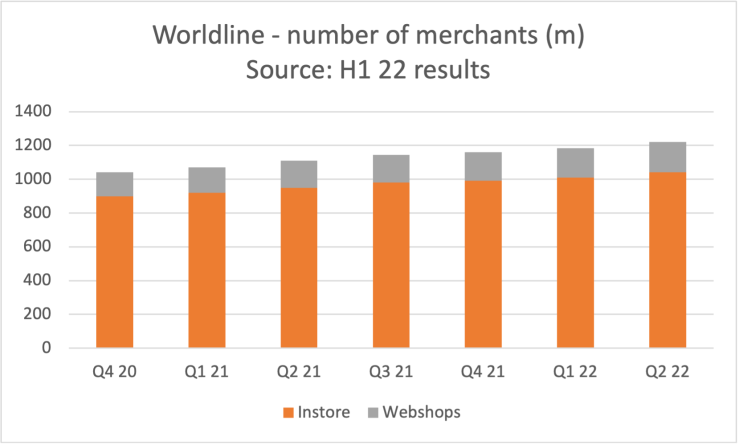

Meanwhile, the bad news for Worldline continues. Belgian prosecutors have launched a money laundering probe, top shareholder SIX is reportedly facing a further $300m loss on its holdings and the ANZ Bank JV in Australia posted grim 2024 results.Worldline Australia made AUD 68m (€42m) operating loss on revenues down 33% to AUD 81m (€49m). The business now needs more capital.

Despite a plunging share price and market cap now under €1bn, analysts aren’t calling Worldline a buy. The bonds are trading at less than 90 cents to the dollar. Rebuilding investor trust will require time, stable results and no more nasty surprises.

GTCR, the private equity firm selling Worldpay to Global Payments, recently explained how it turned the business around in just 18 months, making $6bn in the process. “Worldpay had the potential to win. It had just lost a bit of its competitive spirit,” said GTCR’s CEO.

Not so fast. The deal has hit turbulence. Activist investor Elliott has taken a stake in Global Payments though its intentions remain unclear. Some speculate it may try to install a new board of directors. Meanwhile, UK competition authorities are circling, as the combined companies would control over 40% of the acquiring market.

GTCR might want to hold off booking that profit just yet.

JP Morgan paid $800m for 48.5% of Greek fintech Viva Wallet in 2022 and announced a 50-person “payments innovation lab” in Athens. But the deal quickly soured and is now tied up in litigation in both Athens and London. In the latest twist, both sides are claiming victory. Despite the uncertainty, Viva seems to be doing well in the marketplace and has started calling itself the First Fintech Bank in Europe.

Figure 1 Photo credit Viva.com

Viva is part of a fast-growing group of well-funded, POS-focused European payment start-ups including SumUp, Flatpay, myPOS World and Dojo – some acquirers, some payment facilitators (PF). Let’s call them the Tap Pack.

Dojo, a London-based acquirer, just raised $190m and is growing rapidly in Spain. From offices in Barcelona and Madrid, it’s hiring 100 new sales consultants on a four-hour workday. Hasta mañana.

SumUp, the Anglo-German PF that reported €1bn revenue and a maiden operating profit in 2024, has postponed its IPO to 2026. Valued at €8bn in its last funding round, analysts doubt that figure will hold in today’s market.

SumUp has also agreed, at long last to support Girocard payments. The move responds to two issues: Mastercard’s phase out of Maestro, and the German savings banks’ launch of S-Cube, a SumUp rival with Girocard bundled in.

Flatpay says it will sign 5,000 new merchants this month, boosted by its French expansion which claims 40 staff and 1,000 merchants already. Pricing is very keen – a free PAX A920 and all transactions at just 1.29%. The Danish PF is entering the UK next with the radical innovation of recruiting an in-house sales team in place of the usual network of self-employed agents.

The Tap Pack have been gaining ground at the expense of incumbents like Worldline and Barclaycard. But they now face pressure from a new wave of capital-light, unregulated startups offering a slick user experience on Adyen’s rails. Examples include Yetipay, Kody, and MyPOS Connect (not to be confused with MyPOS World).

London-based Yetipay just raised £3.5m in debt and equity for its hospitality payments platform. It claims to process £500m annually and generate £5m in revenue. The Adyen integration has enabled fast expansion into Spain and Italy. Here’s a photo of founder Oliver Pugh with what the press release questionably describes as a pink yeti.

Turning to SoftPOS, Rubean, listed on the Munich Stock Exchange, is finally seeing real growth. First-half 2025 revenues jumped to €2.54m, up from €0.84m a year earlier. Analysts expect full-year sales to double, and the stock has surged 35% to an all-time high of €8.75.

Rubean’s key selling points include Girocard support and integration with Redsys in Spain. Deichmann, the German shoe retailer, uses Rubean’s technology on Zebra handhelds into payment terminals. It’s a great example how SoftPOS can be transformational for enterprise retail.

In fundraising news:

- Modern World Business Solutions (UK) raised £9m to scale from 60 to 200 staff. MWBS offers a white-label ISO-as-a-service platform and a comparison tool for SMEs seeking better payment deals.

- Ontik, a London-based startup automating cash collection for the building trades, raised $3.7m. Payments are processed via Stripe or Yapily for open banking.

- Paddle, the merchant-of-record platform for SaaS vendors, shrugged off a recent $5m US regulatory fine with a $25m debt raise. Its 2023 accounts showed a £46m operating loss on £57m revenue.Germany’s savings banks remain rare incumbent winners. S-Payment, their merchant services arm, grew revenue 13% to €292m in 2024, with mobile payments (Apple/Google Pay at POS) especially strong. Girocard transactions rose 12%, double the national average. And no red flags were raised in PayOne, the group’s JV with Worldline—which will reassure its beleaguered shareholders.

Scheming

Visa and Mastercard are facing mounting legal pressure in Europe. In a landmark UK ruling, a court found that commercial and inter-regional interchange fees breach competition law. Crucially, the court ruled interchange is anti-competitive “by object” – a first which could trigger a wave of merchant damages claims. Both networks plan to appeal.

In Switzerland, major retailers are seeking damages over “unlawfully charged fees,”arguing boldly that card payments should be free. Meanwhile, the Swiss Retail Federation has referred Twint, a mobile payment solution owned by the domestic banks, to regulators, claiming its merchant fees are even higher than credit cards.

Visa and Mastercard justify their fees by highlighting innovations such as tokenisation, now covering nearly half of Mastercard’s European transactions and Click to Pay, their long-delayed answer to PayPal. This is finally getting some serious marketing dollars although these don’t seem to have reached Poland.

With European payment sovereignty high on the political agenda, much depends on wero, the wallet backed by the European Payments Initiative (EPI). According to Finanz-Szene, EPI has raised an impressive €450m from shareholders including Worldline and Nexi. To succeed wero needs wide distribution through mobile banking apps and broad acceptance from merchants.

The distribution side is going well with five new Belgian banks added and Austria reportedly in talks. Wero claims 42 million users across Belgium, France, and Germany and processed €5bn in P2P volume in its first three months. eCommerce support is due this year, with in-store payments in 2026.

iDEAL, the Dutch online payment method set to be folded into Wero in 2026, grew merchant volume 13% to €100bn in 2024. while overall debit card spend rose just 3%.

Wero hopes to link with Europe’s domestic mobile wallets, including Blik (Poland), Bancomat (Italy), Bizum (Spain), Vipps (Norway), IRIS (Greece), and MB Way (Portugal). Greece’s IRIS is likely to gain momentum thanks to a new law mandating acceptance both online and in-store.

Blik continues to dominate in Poland, reaching 70% share of eCommerce in Q1. Online volume rose 31% to €12bn. Backed by Mastercard, Blik’s bank shareholders are eyeing cross-border growth. The CEO of PKO BP has urged Central European players like Raiffeisen, UniCredit, and Intesa Sanpaolo to join the Blik consortium.

ISV

The convergence of software and payments, pioneered in the USA, is now accelerating across Europe. A new report from Flagship Consulting highlights the extent to which PSPs are acquiring European software firms to gain distribution in key verticals like restaurants and retail. Let me know if you spot any they’ve missed.

American software vendors realised years ago they could double their margins by integrating payments. As Jim Roddy from the Retail Solution Providers Association puts it: “ISVs are the new ISOs. “I visited an RSPA member once, and the CEO didn’t show me new software. He shut the door, plugged in a TV, and pulled up a spreadsheet showing how much he made monthly from payments. The numbers were huge.”

Not all customers are thrilled. American restaurateurs are increasingly frustrated at being locked into inflexible, expensive payment setups bundled with their POS software. While competition authorities haven’t stepped in yet, scrutiny may not be far off, especially if merchants are barred from choosing their processor.

Acquirers hoping to partner with ISVs need to fully embed their offer within the software vendor’s customer proposition. That means API-based onboarding, access to management info, smooth customer service, transparent pricing, and generous commissions for the software partner.

Where does it go wrong? A Dutch restaurant shared on LinkedIn its experience of switching from Worldline to Viva. Integrating Viva’s terminals with its Odoo ECR software took less than two minutes. Worldline supports Odoo too but only via a special IoT box costing €35/month. The restaurant chose Viva despite higher transaction fees, citing better support and a simpler setup.

Agentic shopping

The public is starting to use ChatGPT and other AI tools for search, and it’s not just Google that should be worried. OpenAI, ChatGPT’s parent company, wants a cut of online purchases made via its platform, posing a margin threat to merchants and commerce platforms alike.

ChatGPT’s prototype shopping agent is slow and error-prone today, but it’s easy to see how it could soon become ubiquitous and render traditional eCommerce websites obsolete. If the AI already knows your shipping and payment info, what’s the point of a checkout page? Simon Taylor explores the implications. Startups like Ogment are already offering tools for merchants to adopt.

Shopify, the world’s leading eCommerce platform, is pushing back, posting a robots.txt file that directs agent developers to its official checkout SDK. Amazon is doing the same. As this LinkedIn discussion shows, Shopify’s move may upset tech purists but will please merchants already overwhelmed by bot traffic.

It’s still early days, and AI can’t yet be trusted. In one test, an AI managing an office vending machine lost money by over-discounting snacks and inexplicably stocking unsellable metal cubes.

New shopping

Walmart removed self-checkout from one store and saw police calls fall 50%, suggesting the public is increasingly non-compliant with “honesty-based” retail. That puts new pressure on AI to deliver smarter automation. Here’s a good roundup on autonomous stores.

Despite Amazon’s recent U-turn, checkout-free tech is gaining traction in high-traffic locations like stadiums. In Europe, we’re seeing rollouts in small grocery formats. Coca-Cola HBC plans 15 checkout-free stores in Hungary using low-cost Chinese AI from Cloudpick, integrated by Kende Retail and with payments by myPOS. This price is said to be just €40,000 for each shop.

Old fashioned vending is also rising as a payments channel. This 72-lane Boxbar drink dispenser in Manchester uses Adyen, Global Payments, and Viva for processing.

Having failed to commercialise virtual reality, Meta is now focusing on augmented reality via glasses and recently acquired a 3% stake in EssilorLuxottica, makers of Ray-Ban. It looks less ridiculous than a VR headset and you can imagine the power of AI seeing what you’re seeing and whispering helpful advice in your ear. Or maybe not. Matt Jones explains what it means for payments.

In Hong Kong, Alipay has launched smart glasses that let users pay by looking at a QR code and speaking the amount out loud. Rokid powers the app. Meizu has a similar product, with a dash of dystopia. People using these glasses don’t make eye contact and it’s very disconcerting as you can see from the video.

Product

Here’s a novel but quite risky idea. Better, based in Tel Aviv, is offering to step in to honour transactions where the card is declined due to insufficient funds. This start-up will “save the sale” by settling the merchant (less 10-15% commission) and waiting until after pay-day to put the transaction through. Better says it has already run a proof of concept with PayU. Similar products are available including Bounce.

App Store vendors can now bypass Apple’s 30% commission by using third-party payment processors. Stripe, much better value at 2.9% + 30c, has published a how-to guide. Apple, unsurprisingly, has responded by placing consumer warnings to scare consumers away from alternative payment options.

Many subscription payment providers are struggling to keep up with the move by software vendors away from per seat or tiered pricing to models focused on how much data you crunch. Stripe reports that this “usage-based” billing is up 145% year to date.

Payments and loyalty

Rewe, the German supermarket giant with 3,800 stores, has launched Rewe Pay, a QR code wallet built by its in-house processor, Paymenttools. Setup is a bit clunky: shoppers register their Girocard, then complete a SEPA direct debit mandate via the app and sign their name on an in-store tablet. After that, payments are easy, made by scanning a QR code at checkout.

Commentators see Rewe Pay as a response to rising processing costs, especially as shoppers increasingly use Apple Pay linked to Visa and Mastercard, but the automatic incorporation of Rewe Bonus points on all purchases is equally interesting.

In a controlled, single-merchant environment like Rewe, the model should work. But I’ve long been sceptical of open-loop, card-linked loyalty. That idea has been around for years but has stumbled on technical barriers, unreliable merchant category code (MCC) data, and the difficulty of building profitable loyalty economics. Plus, card-linking offers benefits after the transaction, not before, making it hard for merchants to recognise high-value customers at the point of sale.

There’s no shortage of casualties:

- Bink burned through £67m despite high profile backers including Barclays and Lloyds banks

- Fidel API lost $60m

- Izicap, a French startup backed by €15m from the European Investment Bank, failed despite partners like Crédit Agricole and Nexi

Still, some players show promise. Krowd, a Techstars-backed London startup focused on restaurants, powers Amex Dining Rewards, has launched with Revolut and has its international expansion backed by Mastercard.

Paylead, based in Bordeaux, takes a bank-centric model, linking consumer ccounts to retail deals at the largest merchants such as Auchan and Decathlon. Paylead raised $6m in 2020. And Loyyo (Netherlands) replaces stamp cards with payment-linked rewards, is available via Adyen and CCV also recently secured new funding.

Fraud update

Chargebacks continue to rise. Ethoca projects global dispute volumes will hit 324 million by 2028, driven mainly by post-sale issues like slow refunds, unclear billing, and delivery friction, rather than outright fraud. The real pain is operational which has pushed merchants to look beyond traditional fraud tools. Visa’s Rapid Dispute Resolution (RDR) is gaining traction and is claimed to cut chargebacks by 20–30% for participating merchants.

So much for the carrot, here’s the stick. Visa’s updated Acquirer Monitoring Program(VAMP) is raising the stakes. Acquirers now face stricter thresholds, tighter enforcement, and the risk of fines, or even losing their membership if chargeback rates across their merchant portfolios climb too high. TrustPay (not to be confused with Trust Payments) has a solid explainer on the changes.

VAMP and Mastercard’s counterpart, the Excessive Fraud Merchant (EFM) programme, put pressure on acquirers and PSPs to take a more proactive role in policing their portfolios. In recent weeks, both Worldline and Paddle have shown the consequences of inattention. But for merchants, the message is equally clear: chargebacks are no longer just a cost of doing business, they’re a serious reputational and commercial risk that could jeopardise access to processing altogether

Car Commerce

The global auto industry is scrambling for new revenue and wants to pivot to a service-led model where drivers pay for parking, charging, or fuel directly through the vehicle’s OS. Naturally, the car brands want a cut. That’s why many are now resisting Apple’s “CarPlay Ultra”, which sidelines in-car payment systems. The problem? Motorists prefer to dock their phones and control everything from there. Top Gear takes a detailed look in this video.

Jas Shah offers a solid overview of today’s fragmented mobility market. For example, the UK alone has over 30 different parking apps, and that’s before you factor in EV charging.

Under pressure from government, the UK industry has agreed to roll out a National Parking Platform which allows any participating app to work across all publicly owned car parks. It’s already live at 476 locations, handling 550,000 transactions a month. There’s not that much money in parking payments. I calculate the three leaders in the UK market – Ringo, JustPark and Paybyphone – generate annual sales of c.£60m between them.

Open banking

UK open banking payments have stalled, with volumes flat at around 28 million transactions per month since early 2025. This reinforces the urgent need for a proper open banking scheme—with an acceptance mark, rulebook, consumer protection, and a business model that gives banks a reason to maintain high-quality APIs.

TrueLayer underscored the slow pace of adoption across Europe with new figures from France and Germany Despite claiming a 60% market share in France, it processes just €2bn annually; in Germany, it holds 30% with €1.4bn in volume. Nobody is getting rich soon. A new Stripe partnership may help, but patchy bank APIs continue to limit growth.

Meanwhile, Trustly appears to be the only open banking player making real money. In 2024, volumes rose 54% to $85bn, and net revenue grew 32% to $239m. “Adjusted”EBITDA was up 50% to $73m. Business remains strong in North America and Europe, where Trustly retained its UK Government tax contract. Note: these results come from a press release, not audited accounts.

Trustly’s profit engine is widely believed to be US gaming, so others are following. London-based Yaspa, which offers open banking payments with integrated KYC, has raised $12m to target US iGaming, through a new office in Atlanta.

In a completely different vertical, Bumper, a UK car finance company, has acquired Cocoon, an open banking payment vendor which says its product is used by 20% of car dealers.

Stable coins

There’s been an explosion of commentary on stablecoins following the approval of Trump’s Genius Act, which for the first time sets out a regulatory framework. Jason Mikula has the details. Genius has triggered a rush among banks, fintechs and retailers to launch their own digital dollars which will be backed 1:1 by US Treasuries, although, unlike dollars in a bank account, there is no deposit insurance.

Why would businesses want in? For one, they keep the interest on Treasury bonds. And for retailers, stablecoin wallets could cut card fees if shoppers preload value. But it’s unclear why everyday users, especially in European democracies with easy access to banking services, would hold a private currency with no consumer protection. “Unless you’re a criminal, there’s no use case,” says Ryan Cummings, former White House advisor.

Business of Payments readers likely have two questions:

- When will stablecoins be used for retail payments?

- Is there money to be made?

On the first: as Jeremy Light shows, most stablecoin activity today is crypto trading. Retail payments? Just $250m/month, nearly all in Tether (USDT). Visa and Mastercard have cited poor user experience and high fees as major barriers to adoption.

As for profitability: probably not. If stablecoins are fungible, meaning a “Walmart dollar” is interchangeable with a “JPMorgan dollar” then margins may collapse to 10bps, in line with money market funds. Coinbase is already offering 4.1% on USDC, and as Andrew Dresdner notes, that leaves little room for profit.

In other news

The latest UK government payments strategy includes the formation of several new committees: a Payments Vision Delivery Committee, a Vision Engagement Group, and a Retail Payments Infrastructure Board. Undoubtedly good news for those who make a living sitting on industry panels.

In aviation news, Stripe is reportedly suing the investors behind Bonza, the bankrupt Australian airline. Stripe processed payments and now faces 70,000 chargebacks worth A$20 million.

In Denmark, NETS went down on Saturday 19 July, leaving Danes unable to use ATMs or POS terminals at home and abroad across Dankort, Visa, and Mastercard. One group of Danes stranded in Cyprus wrote: “Our plan for now is to try a live performance that includes both singing and dancing, but we are crossing our fingers that the problem is resolved before they refuse to serve us any more beers.”

Figure 2: Danes struggling to come to terms with the NETS outage

Romania is the latest country to introoduce an industry-backed push to increase card acceptance at small businesses. The ePOSibil programme, backed by Visa and six local banks, offers six months of free terminal rental.

Sifted’s new list of top European B2B SaaS firms includes four from the payments world: infrastructure players Primer (London) and Payrails (Berlin), as well as Brite(open banking, Stockholm) and Sunday (restaurant pay-at-table).

In the US, a court has struck down the Federal Trade Commission’s proposed “click to cancel” rule, which would have required businesses to make cancelling subscriptions as easy as signing up. The rule was fiercely opposed by lobby groups and now looks to be off the table.