Worldine’s H2 results underlined how much progress the Paris based organisation has made towards establishing itself as “as a premium global Paytech at the heart of the European payment ecosystem.” Originally spun out of ATOS, primarily as a back office processor, Worldline has reinvented itself. Merchant services now accounts for 68% of group revenue.

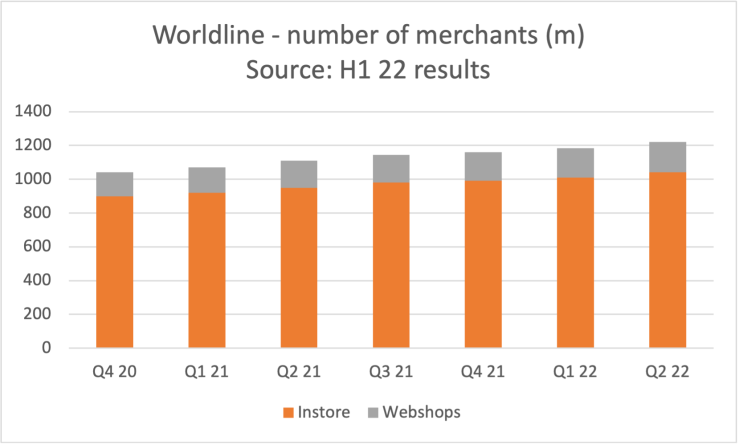

Payment volume was up a very impressive 30% in H1 to €177bn as the impact of new acquisitions kicked in. The positive result was also “reflecting the widespread and rapid shift towards digital payments.”. Organic growth has been positive too and Worldline is adding roughly 10,000 new merchants each month split pretty evenly between in-store and online. Total merchant count now exceeds 1.2m.

Revenue from merchant services grew 16.8% “fuelled by steady growth in commercial acquiring across all geographies and customer segments” with acquiring growing faster than its payment acceptance or digital business lines. Acquiring delivered “strong double digit growth trending towards 30% with almost all geographies and customer segments contributing…. and a strong performance from DCC products and the positive impacts from strong holiday period boosting the Travel and hospitality verticals.” Much lower growth – mid to high single digits – was reported from payment acceptance (mainly payment gateways and managed POS terminals) and digital services.

The wholesale business fared a little less well as a number of ex-Equens contracts were renewed on less favourable terms although Worldline did re-sign Credit Agricole for a new five year deal, And it started working with AEGON Bank for SEPA instant processing. Overall, higher authentication volumes related to SCA compensated for lower iDeal volumes in the Netherlands.

Highlighting Worldine’s ability to win new bank partnerships, three big acquisitions closed in the half year.

- Italy – acquired an 80% share of BNL’s merchant acquiring business in Italy. Known as Axepta, this JV brings c. 5% market share including 30,000 merchants with 220,000 POS terminals and 200m card transactions annually. Enterprise value was €220m.

- Greece – acquired an 80% share of Eurobank’s merchant acquiring business in Greece which brings a 21% market share including 123,000 merchants with 190,000 POS terminals, 219m transactions and € 7bn of payment volume. This acquisition complements Cardlink, the leading Greek network service provider (NSP) which Worldline bought last year for an enterprise value of €155m. The vertical combination of NSP and acquirer under common ownership is likely to accelerate consolidation of the fragmented Greek retail payment market which has recently become the focus of much international investment.

- Australia – went live with its joint venture with ANZ. Worldline holds 51% of the new business which brings 80,000 merchants and 2bn transactions pa. Worldine has pledged to spend $22m AUD to localise its platforms for Australia.

Beyond banking, Worldine announced a slew of large merchant wins and new distribution partnerships. These included retailers such as JD Sports and Jysk but also high-risk merchants in the travel sector – TUI Cruises and Iceland Air. New partnerships include Planet Payments (DCC and tax free shopping) and Casio (integrated payments in Japan). More interesting for the future, was the launch of a new Softpos product in Belgium working on the Softpos.eu platform. Worldine has been working with Softpos.eu – a very well regarded start-up – in Poland since 2020 and clearly now sees the proposition as ready for international roll-out.