Improving conditions for international travel boosted spending on Discover’s Global Network in Q2.

Discover is the third card brand in the USA, a long way behind Visa and Mastercard, but very profitable nonetheless. Discover bought Diners Club International from Citbank in 2008 which gave it the basis of a global acceptance network. Diners cards are still issued in various countries by franchise partners although not so much in Europe these days. For example, the Diners Club franchise partner in Poland recently announced it was exiting the market.

Discover has continued to invest in growing its international acceptance through deals with merchant acquirers and local debit schemes. More than 25 other networks, issuers and fintechs access the DGN rails to give their customers the ability to use their cards internationally. The latest partner is Bancomat which was announced in June 2022. When implemented, this alliance will allow cardholders access to the Bancomat acceptance network in Italy.

Diners volume was up 37% year-on-year in Q2 to $8.4bn “reflecting improvement in global T&E spending.”

Network partners volume was up 22% to $11.5bn “driven by higher AribaPay volume.” AribaPay is a collaboration between SAP and Discover in North America for B2B payments.

Roger Hochschild, CEO, said that he remained “committed to expanding our international merchant coverage… We see a lot of value from the network, not just in the Payment Services segment, but for the differentiation and capabilities it gives our card issuing business, and in particular, the support it provides for rewards on debit, which is a real differentiator in the marketplace.””

Euronet’s merchant payments and ATM business continues its strong rebound from the pandemic but management warned that the ongoing disruption to European travel would be a restraint on growth into H2.

Euronet is headquartered in Kansas but does most of its business outside the US. Overall revenue was up 18% in Q2 to $843m. The epay and Money Transfer divisions must be giving cause for concern with sales down 7% and up just 3% respectively but it’s the EFT Processing division which interests us at Business of Payments.

EFT Processing revenue rose 119% from $113.5m to $249.0m. 80% of this is made in Europe.

All metrics have moved strongly in the right direction. More transactions and more high margin transactions have been flowing through Euronet’s processing centres. Total transactions (POS + ATM) were up 59% at 1.573m while revenue per transaction grew 45% to $0.16. This reflects “the higher proportion of high value and high margin DCC transactions due to reduction of travel restrictions.”

Heading into the second half of the year, management called out several headwinds including strengthening USD, rising interest rates, inflation and staffing/operational issues in the travel industry. Michael Brown, CEO was particularly harsh on Heathrow.

“Let’s not forget, travellers from the U.K. are by far the largest producer of high-value international transactions on our ATMs because every card has a cross currency component. So, the limiting of passengers to and from the British airports has had a more significant impact on our forecast.”

Euronet manages a total of 51,062 ATMs, some directly and some on behalf of 3rd party operators including banks. ATM’s were particularly badly hit by the pandemic but, despite early forecasts of the death of cash, have bounced back strongly in the recovery. Total number of ATMs grew 10% boosted by deals in India, Spain (with the Post Office to provide access to cash in rural locations) and a new independent network in Iceland. Revenue per ATM grew from $934 to $1696.

Future deployments have been hit by operational problems. “We have been challenged with supply chain issues related to our ATM deployments. These issues range from manufacturers not delivering the machines on time to third-party resource issues installing them.”

In addition to the ATM’s, Euronet manages 570,000 POS terminals, mainly as an outsourced provider to banks. However, it took direct control of its estate in Greece during Q2 through the acquisition of the merchant services division of Piraeus Bank. This gives Euronet an estimated 40% share of the Greek POS merchant acquiring market and 20% of eCommerce. According to Euronet, new business is healthy – 5,000 merchants were signed in Q2 including some marquee names such as Ikea and TGI Fridays – and the transition to Euronet’s platform “has gone smoothly.”

EFT Processing is highly geared. Revenue more than doubled but operating expenses rose just 40% which helped operating income swing into $54.8m profit from a loss of $25.3m in the same quarter of 2021. Investors will be hoping this rebound has further to go. Even at the new profit level, operating income margin in this division is just 7% and return on assets 4.1%.

PagoNxt reported very positive sales in H1 2022 as its core markets of Spain and Latin America continued to recover strongly from the pandemic.

Unlike some banks, Santander regards payments as strategic and formed PagoNxt to consolidate all its merchant payment assets in one ring-fenced organisation. The merchant facing brand is GetNet.

Rather than build the technology to link its national assets and attract cross-border merchants, PagoNxt bought Wirecard’s platform from the administrators in 2020. It’s too early to know whether this bet has paid off – platform migration is a notoriously tricky business – but the purchase does allow PagoNxt to win at buzzord bingo. Who could resist its new “global, cloud-native, data-driven… connected, retail-time, flexible and highly scalable technology platform that is fully cloud and API-based…”

Back to the H1 results and global payment volume was up 35% to €74.6bn. European volume was up 53%, Mexico by 38% and Brazil by 23%. The strong European performance was driven by “exposure to high growth verticals in Spain” which very probably means the rebounding tourist market. PagoNxt is now present in nine European markets (including the UK where Santander’s payment presence has always been weak) and is investing in “targeting specialised industries including airlines and mobility.”

Total merchant count grew 5% year on year to 1.27m including 20,000 selling cross-border. Payment volume per merchant grew 29% in the half year to an annualised €118,000. European merchant count increased 15%.

Revenue was up a very healthy 87% to €398m with the take rate rising 16bps to 0.53%. Expense grew just 43% to €447m which resulted in narrowing losses to €50m from €108 in H1 2021.

Commentary on Klarna’s H1 results focused on its ballooning losses and the uncertain outlook for BNPL as we enter tighter credit markets. Klarna has reacted by cutting staff and scaling back investment plans. Consumer credit is outside our scope at Business of Payments but the merchant side of Klarna’s business is still a very profitable operation.

Total gross merchandise volume was up just 5% year on year to $41bn for the half year.

The US and UK are “the main drivers of volume growth”, up 109% and 70% respectively. More of the top 100 US retailers take Klarna than either Affirm or Afterpay. Of course, all the top 100 take Visa, Mastercard, Discover and, very probably, Amex and Paypal too. Competition for “top of wallet” is fierce and not just in the US as you can see from JD Sports’ checkout below. It’s going to take a great many marketing dollars to persuade shoppers to keep clicking on your logo rather than one of the other options.

Net operating income was up 12.3% at $872m. The positive result masks a 7% fall in dollar terms in Germany and a 20.8% decline in Sweden, Klarna’s home market. With its more mature markets going backwards, there is clearly a worry that the proposition has a shorter runway than management had hoped.

One of Klarna’s strengths should be the operation of a two-sided business model. It makes money from charges to both merchants and shoppers. Net operating income from its 450K retail partners grew 8.6% to $467m in H2 while that from 150m consumers fell 9.1% to $293m. This works out as $1038 from each merchant but just $2 for each consumer. Klarna is making much more from merchant payments than consumer credit. Take rate from retailers (operating net income/GMV) was a very healthy 1.14% in H2.

Klarna was profitable until 2019; its business model brilliantly conceived to help merchants in Sweden and Germany digitise the slow and risky processes of invoice payments. Klarna’s innovation was to take title to the goods at checkout. Conversion rates went up and merchants’ credit losses went down. Happy days.

It’s now clear that this model has been difficult to export profitably to card payment markets including the UK and USA. Klarna has been forced to adapt by focusing less on merchants and more on building a consumer brand equal to the superapps which have proved so popular in the Far East.

The Klarna App now includes price comparison, stock checking, offers and retailer promotions. Of the 150m Klarna users, 23m have the app and growth is reportedly strongest in the USA. New features announced in H1 include video links with product experts at leading brands and an in-app loyalty digital wallet allowing access to 8,000 loyalty and reward programmes worldwide with no need for plastic cards. None of this development comes cheap.

Klarna believes that its app drives consumers to visit retailers (both online and F2F) and that it can charge merchants for the additional footfall. Marketing services revenue was up 200% in the half-year although the dollar revenue was not disclosed.

Interestingly, Klarna has built an in-house openbanking API aggregator and is now commercialising the capability to 3rd parties as Klarna Kosma. This is a crowded field but Klarna does have the benefit of a proven A2A technology team at Sofort, the German bank payment specialist it acquired in 2014. Kosma is believed to be running at 200m/tx per annum with customers including SIBS (Portugal) and Airbank.

Paysafe’s new CEO, Bruce Lowthers (ex FIS), has begun the turnaround of the underperforming payment processor promising a “laser focus on accelerating sales, innovative product delivery and operating at speed.” Commenting on the Q2 2022 results, Lowther said that the “organisation [is] still too complex and is operated in silos.” In product innovation, “bluntly, we have lost our way”. Lowthers was particularly critical of a failure to invest in its consumer-facing wallets, notably Skrill and Neteller.

Lowthers believes Paysafe’s unique selling point should be its two-sided business model and its ability to connect 250K merchants with 15m consumer wallet users. He sounded optimistic for the medium term when promising to simplify the organisation with new leadership appointments that would bring customer-focus to the investment challenges ahead.

Meanwhile, guidance for H2 was revised lower. Management cited the Ukraine war, the strong dollar/weak Euro and European gambling regulations alongside softer activity in financial markets and crypto trading.

Paysafe was formed by the merger of a European high-risk business with a background in consumer wallets used to fund gambling and gaming accounts, and a US acquirer with a heritage serving more conventional high street small businesses. Revenue is split 48% North America and 40% from Europe.

The US SMB business is doing fine. But the European merchant services and consumer-facing wallets remain under severe pressure. One analyst wondered out loud whether “the merchant acquiring business in the US should be separated out, given the potential valuation opportunity in some of those businesses.”

Total payment volume in Q2 was up an anaemic 3% year on year to $33.4bn. The two sides of the business reported very different numbers. US acquiring volume was up 8%, boosted by “continued strength in US SME retail,” notably restaurants, retail and petrol. In contrast, the digital commerce division, which includes e-wallets and European merchant processing, saw volume fall 5%.

Total revenue was down 1% to $378.9. US acquiring sales were up 14% while digital commerce fell 13%. e-wallet revenue continues to decline and dropped 19% year on year. Even revenue from European integrated and eCommerce solutions was down 4%. That’s a very poor performance in a merchant payment market still generally seeing healthy double digit revenue increases.

The company has a good position in gaming. US regulated iGaming revenues were up 70% as new markets open up. Paysafe recruited its first operators in Ontario and Arkansas. Ohio is coming later this year. On the other hand, the European gaming market, which is larger and longer established, has weakened as tighter regulations kick. Worse for Paysafe, its e-wallets and e-cash products are under pressure from alternative funding mechanisms such as account to account.

Company specific factors apart, one reason for Paysafe’s problems is that it is highly exposed to the sort of digital merchant that prospers in good times but is vulnerable when consumers hold back discretionary spending. 80% of revenues are from what Paysafe describes as “entertainment” including the likes of Binance, Spotify and Fortnite.

Adjusted EBITDA, the company’s preferred profit measure, fell 13.4%. US acquiring was up 30% with margins up 3600bps but digital commerce down 25% with margins falling 590bps. Capex ticked up 40bps to 6.4% of revenue.

Net income before exceptionals fell from $66.4m to $37.5m but the full picture was much worse. Safecharge booked a net loss of $631m after a “non cash impairment charge” of $676m due to “due to a sustained decline in Paysafe’s market capitalization, as well as current market and macroeconomic conditions.” If anyone can explain why a company takes a charge due to a fall in its own stock price, please let me know.

Nuvei disappointed investors with its Q2 results. Despite healthy growth in processing volume, margins narrowed and the company lowered its guidance for the remainder of 2022. Headwinds include “volatility in digital assets and cryptocurrencies and caution with regard to global economic conditions.”

The company was formed in 2019 when the original Nuvei – Canadian listed and focused on SMBs in North America – acquired Safecharge, a UK listed Israeli acquirer/processor with strength in high-risk sectors such as gambling and gaming. The merger gave Nuvei international exposure and a strong foothold in some of the fastest growing eCommerce verticals.

Three years on, Nuvei now claims global availability of all its capabilities from a single API. This allows merchants to access all they need on a single stack rather than using different vendors for acquiring, gateways, fraud prevention tools and business analysis/reconciliation software. Smaller, fast growing, internationally minded merchants will find this one stop shop approach attractive.

Global payment volume was up 37% to $30.1 bn in Q2 with c.$4bn from POS transaction. Take rate fell 11bps to 0.71% although remains very healthy reflecting the proportion of high-risk business in Nuvei’s portfolio.

Revenue was up 19% to $211.3m. Strong growth in EMEA (+28%) and Latin America (+29%) was offset by underperformances in North America (+8%) and Asia Pacific (-45%). “New business in the regulated online gaming vertical is progressing well” and there has been evidence of cross-selling between customer bases in Europe and North America, and between eCommerce and POS.

Adjusted EBITDA, the company’s preferred measure of performance, was up 17% to $92.9m with margins falling by 100bps to 44%. Staff numbers grew a further 100 to 1,570.

Net income was down 10% to $35.5m hit by a generous $27.7m increase in share-based payments to employees joining from newly acquired companies. Capex rose from 4% to 6% of revenue.

In a busy quarter for product news, launches included:

Enhanced and expanded payout options. These are critical in winning and retaining gambling merchants. New features include SEPA Instant in Europe and Visa Direct in Canada.

A new “Nuvei Simply Connect” SDK will make it easier for merchants to integrate their shopping carts/CMS with Nuvei’s front end.

Omnichannel availability “with a single integration” covering multiple channels and multiple geographies including unified tokens. New customers include Canadian eco-rain gear brand Hatley that will use Nuvei for in-store payments at 40 retail outlets in North America as well as online processing for sales in Europe.

A further 20 Alternative Payment (AP) types to bring the total to 570. This sounds impressive but AP’s are not really a numbers game and, unless they bring significant volume, can quickly put pressure on overheads.

Adyen’s share price took a knock after H1 results as investors were unimpressed at a sharp reduction in margins. The business is growing faster than ever but incremental payment volume is delivering diminishing revenue. The extra €46bn processed in H1 (over H2 21) produced an additional €43m revenue (a take rate of just 9bps) and zero EBITDA.

Management insisted that no customers are loss-making and that it was still “onboarding profitable volume at scale” and that “there is strong operating leverage in the business.”

Overall, payment volume grew 60% year on year to €346bn with the recently established POS business up 97% to €45bn as Adyen grows its share of multi-channel retailers. On the results call, Ingo Uytdehaage, CFO, assured analysts of continued progress. Adyen is in a “fast growing space and our runway is significant.”

The declining take rate was explained by a number of factors including a rebound in airline volume (for which Adyen only provides gateway services) and tiered pricing which offers discounts to enterprise merchants as their volume increases. More positively, existing customers seem happy. Churn remains <1% and current merchants are providing 80% of the volume growth. This indicates how well Adyen has positioned itself as the go-to provider for many of the most successful digital businesses.

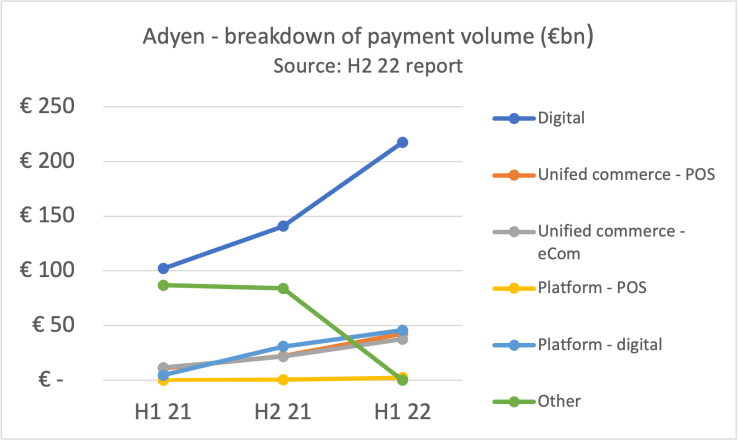

Adyen has divided its business into three segments – Digital, Unified Commerce and Platforms.

Digital includes merchants trading purely online. Volume more than doubled from €102bn to €218bn.

Unified Commerce includes merchants trading both POS and eCommerce. Volume was up from €22bn to €80bn of which POS now accounts for more than half. Adyen says it wins business because of its single platform which allows it to “translate the most complex consumer demands into seamless shopping journeys such as self-checkout, cashierless stores and buy-online-return-in-store.” New customers include Dior, All Saints and Uniqlo.

To help deliver a better customer experience, Adyen has taken the unusual step of commercialising its own design of payment terminals. Two were announced alongside the financial results – a PINpad which connects to smartphone or tablet and a more highly configurable Android terminal which can run ECR and payment software on same device. Hardware is a means to an end. The CFO explained the aim “is certainly not to increase profits on the terminal hardware side. It’s more on the innovation side and making sure that … by having full control that we could drive down the cost of the terminal.” Adyen is also one of small number of vendors working with Apple on launching SoftPOS in the US.

Platform includes marketplaces and ISV. Volume grew 53% to €48bn. Platform is Adyen’s strategy to address the high-margin SME market through partnerships although the volume is suspected by some commentators to be mainly coming from eBay – a customer Adyen won from Paypal.

Adyen has developed a broader range of financial services to sell to SMBs through its platform relationships – business bank accounts, loans and card issuing – but these are “still in beta” and for the foreseeable future, it does not expect significant financial contributions.” The CFO explained “it’s going to take a couple of years to really see the revenues.”

Net revenue was up 37% to €608m with strong performances from APAC and North America. Revenue growth of 30% in EMEA probably indicates Adyen is not gaining share as fast as previously. EMEA remains the largest market and accounts for 57% of total net revenues.

EBITDA was up 31% year-on-year to €356m but actually declined slightly from H2 21 to H1 22. Overall margins remain a very healthy 59%. Profits were hit by higher payroll costs as 395 staff were added, together with a sharp increase in travel as employees got back on the road to meet customers and each other. Adyen made a very clear commitment to F2F business life: “It’s clear that building trusted relationships and driving innovation moves faster when time is spent together. The speed and excitement that meeting each other in person brings has always been a crucial part of our success and our view on how to build the Adyen culture for the long term.”

Capex was €40m (up 160bps to 6.6% of net revenue) as a result of the geopolitical crises. “We invested in our data center infrastructure at a larger scale than we would have under different macroeconomic circumstances.”

Nexi reported strong growth across all markets as Europe’s economies bounced back from last year’s Covid lockdowns. Payment volume was up 18% overall powered by resurgent spend in travel and tourism with a particularly strong transaction flow from foreign cards used in Italy.

The geographical performance was mixed. Payment volume was up 13% in DACH, 18% in Italy and an impressive 33% in the Nordics. Italy – Nexi’s home market – accounts for 57% of the total.

Merchant Services and Solutions is Nexi’s largest division – just over half of total revenue – and sales grew 16% to €431m. The detailed picture was far from uniform. For example, SME’s outperformed corporates and eCommerce growth was restrained by recent standards.

Within Merchant Services and Solutions, SME volume grew 38% with DACH and Poland notably strong. The terminal base grew an impressive 150K year on year and we can see the emerging outlines of a good, better, best product strategy featuring:

SoftPOS – recently launched in Hungary (in-house developed by Nexi, distributed by Unicredit) and a Nordic version working with Softpos.io. An Italian launch is in preparation

Smartpay – commercialised by Concardis in Germany, a simple SME proposition to accept Giro and international cards with a PAX A920, online sign up and nice digital portal

SmartPOS – a more highly configured SME terminal with an associated app store provided by Poynt which will be attractive to larger merchants and ISVs

eCommerce volumes grew 19% with attention drawn to the launch of Nets Easy – a simple proposition of payment gateway, reconciliation and payouts under a single contract. Large and key account volumes grew 17%. An interesting detail was that SoftPOS for retail and hospitality “showing good progress” which backs up the growing consensus that micromerchants will not be the primary target for this new technology. Significant partnerships were announced with Global Blue (hospitality and retail) and Zuora (subscriptions).

Like its competitors, Nexi is expanding its footprint through acquisitions and seeking synergies through platform consolidation. Three acquisitions are expected to close in the second half of the year totalling an additional €22bn volume:

Italy – BPER and BdS merchants which brings €13b payment volume, 110K merchants and 150K POS.

Like every other processor, Nexi is increasingly focused on ISVs as a distribution channel and showcased a new partnership with Microsoft in which it becomes preferred European digital payment partner of the American software giant. This looks like a quid pro quo for Nexi selecting Microsoft Azure to accelerate its platform consolidation. In other ISV news, Nexi has taken full control of Orderbird, a Berlin-based restaurant ISV in which it inherited a minority stake from Concardis in a deal estimated at c.$140m.

Pennsylvania headquartered Shift4 announced that it remains on track for Q4 closure of its acquisition of Finaro (formally known as Credorax), the Israel/Malta based high-risk acquirer.

The $525m acquisition will give the domestic-focused Shift4 the capability it needs to position itself as one of the small number of global acquirer/processors. Although Finaro’s payment volume is just $15bn, it brings a full featured cross-border platform including 170 APMs and the ability to settle in over 20 currencies. Beyond Europe, Finaro also has licenses in South East Asia and Japan.

One key driver of the acquisition is Shift4’s relationship with Starlink which, it says, could net $100bn in subscription payment volume. The five-year deal with Elon Musk’s satellite broadband start-up requires Shift4 to provide payment acceptance worldwide. Other synergies include access to Finaro’s 150 person R&D team, launching Shift4’s SMB software in Europe, cross-selling US processing to Finaro’s European gaming clients and “building an integrated payment offering for European hotels and restaurants.”

Not all Finaro’s customers are welcome. Shift4 stated that “merchants representing a negligible amount of volume that are inconsistent with our values … will be phased out upon closing.”

Much commentary on Block’s Q2 2022 results focused on its quixotic Bitcoin strategy but there was also news of its steady progress upmarket and away from reliance on the US.

International gross payment volume (GPV) processed grew 45% compared with 22% in the US, with revenue up 78% to $257m. International gross profit doubled to $98m including a maiden contribution from BNPL and now accounts for 12% of the global total. Excluding BNPL, international gross margin grew 40% to $67m.

Product launches continue apace, as you’d expect from a business spending an eye-popping $512m on product development in the quarter. Block launched 44 products “across our international markets in the first half of 2022 making significant progress on closing product parity gaps while also launching new markets.” This included Square Register in Ireland and Square for Retail in France and Spain.

The proportion of GPV from larger merchants (across all geographies) continues to grow and almost 40% is now accounted for by those processing over $500K per annum.

Meanwhile, in filings at Companies House, Block revealed that UK revenue rose by 110% in 2021 to £25.1m. Square Loans – a merchant cash advance product in which repayments are scaled to a proportion of card payments received – will be launched in 2022/3.