New CEO, Bruce Lowthers, declared himself happy with the first five months of Paysafe’s turnaround. Announcing Q3 results, he said he was so pleased with progress that “I personally purchased 1.2 million shares of Paysafe stock on the open market.”

Paysafe was formed by the merger of a European high-risk business, with a background in consumer wallets used to fund gambling and gaming accounts, and a US acquirer with a heritage serving more conventional high street small businesses. Lowther was hired following a series of profits warnings related to Paysafe’s digital wallets including Neteller and Skrill.

Lowther thinks Paysafe has been its own worst enemy. An over complicated organisation built around product silos has been “leaving money on the table.” In response, the new management has introduced global sales teams structured around customer segments which Lowther expects to “greatly increase our global pipeline and average deal size.” Similarly, all payment acceptance products are being brought together in a new merchant solutions business unit.

The new global verticals are iGaming, retail/hospitality, streaming/online gaming, travel & entertainment and digital assets. The latter may be short-lived given recent market developments.

Questioned on Paysafe’s exposure to crypto currencies, Lowther explained “We’ve got a nice little crypto business… Binance is a great customer. We’ve had them for a little while, and we provide a private label wallet for them.” Alex Gersh, the new CFO, seems less excited, saying “overall, the crypto business that we have is less than 3% of our overall revenue base.”

The updated organisation is expected to accelerate cross-selling merchant acquiring/processing and wallets to the respective customer bases but also make it simpler to follow customers into new geographies. Examples given include Q3 successes of launching “with 10 merchants from Paysafe portfolio into Latin America, including with Bet365 in Mexico.“

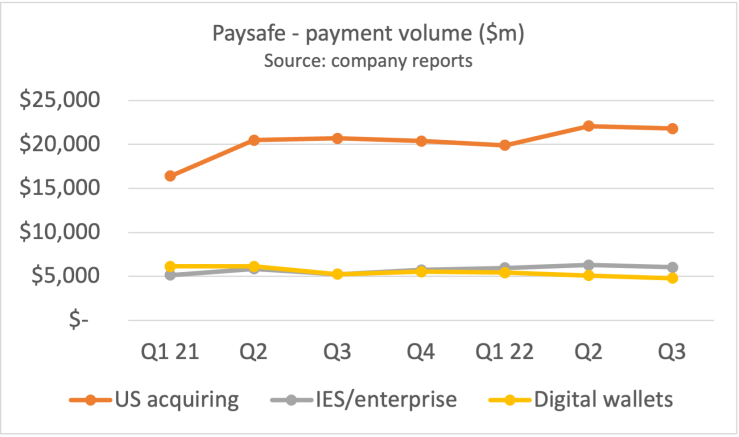

Although investors are clearly reassured that the company has its financials under control and will be holding to full year guidance, Paysafe continues to underperform. In Q3, global payment volume was up a relatively modest 5% at $32.5bn.

Total group revenue grew 4% in the quarter to $366m and adjusted EBITDA was down 10% to $95m as overall margins contracted 4ppt to 27%. Net income showed a token $1m profit.

Looking at the subsegments, US acquiring grew its payment volume just 5% to $28.8bn. This was helped by “continued strength in small businesses” although the overall result indicates Paysafe has lost market share. More positively, the unit shows very strong operational leverage. US acquiring revenue rose 12% to $185m and EBITDA was up 24% at $50m as margins expanded 2ppt. Take rate rose 5bps to 0.85%.

The enterprise acquiring and gateway division (IES), which will now be managed together with US acquiring in the new merchant solutions unit, is seeing considerable challenges. Despite 15% volume growth to $6.0bn, take rate fell 12bps to just 0.3%. The result was a 17% decline in revenue to $18m with adjusted EBITDA swinging to $5m loss from $4m profit in the same quarter of 2021.

The Digital Wallet division was the cause of Paysafe’s recent troubles. The good news is that business has stabilised as “strong momentum in regulated iGaming and Latin America was partially offset by “continued softness” in Europe. Despite volume down 9%, revenue was just 3% lower than the same quarter of 2021 and did grow a little at constant currencies. Adjusted EBITDA was down 11% to $68m but management says that investments in improved customer experience are beginning to pay off. The company is opening 100K new wallet accounts each month on average and consumer funding has begun to rise – up 2% y-o-y in constant currencies.