Adyen’s share price took a knock after H1 results as investors were unimpressed at a sharp reduction in margins. The business is growing faster than ever but incremental payment volume is delivering diminishing revenue. The extra €46bn processed in H1 (over H2 21) produced an additional €43m revenue (a take rate of just 9bps) and zero EBITDA.

Management insisted that no customers are loss-making and that it was still “onboarding profitable volume at scale” and that “there is strong operating leverage in the business.”

Overall, payment volume grew 60% year on year to €346bn with the recently established POS business up 97% to €45bn as Adyen grows its share of multi-channel retailers. On the results call, Ingo Uytdehaage, CFO, assured analysts of continued progress. Adyen is in a “fast growing space and our runway is significant.”

The declining take rate was explained by a number of factors including a rebound in airline volume (for which Adyen only provides gateway services) and tiered pricing which offers discounts to enterprise merchants as their volume increases. More positively, existing customers seem happy. Churn remains <1% and current merchants are providing 80% of the volume growth. This indicates how well Adyen has positioned itself as the go-to provider for many of the most successful digital businesses.

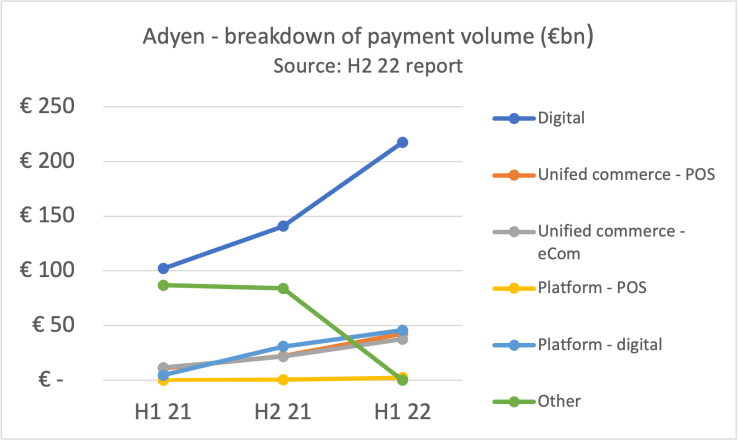

Adyen has divided its business into three segments – Digital, Unified Commerce and Platforms.

Digital includes merchants trading purely online. Volume more than doubled from €102bn to €218bn.

Unified Commerce includes merchants trading both POS and eCommerce. Volume was up from €22bn to €80bn of which POS now accounts for more than half. Adyen says it wins business because of its single platform which allows it to “translate the most complex consumer demands into seamless shopping journeys such as self-checkout, cashierless stores and buy-online-return-in-store.” New customers include Dior, All Saints and Uniqlo.

To help deliver a better customer experience, Adyen has taken the unusual step of commercialising its own design of payment terminals. Two were announced alongside the financial results – a PINpad which connects to smartphone or tablet and a more highly configurable Android terminal which can run ECR and payment software on same device. Hardware is a means to an end. The CFO explained the aim “is certainly not to increase profits on the terminal hardware side. It’s more on the innovation side and making sure that … by having full control that we could drive down the cost of the terminal.” Adyen is also one of small number of vendors working with Apple on launching SoftPOS in the US.

Platform includes marketplaces and ISV. Volume grew 53% to €48bn. Platform is Adyen’s strategy to address the high-margin SME market through partnerships although the volume is suspected by some commentators to be mainly coming from eBay – a customer Adyen won from Paypal.

Adyen has developed a broader range of financial services to sell to SMBs through its platform relationships – business bank accounts, loans and card issuing – but these are “still in beta” and for the foreseeable future, it does not expect significant financial contributions.” The CFO explained “it’s going to take a couple of years to really see the revenues.”

Net revenue was up 37% to €608m with strong performances from APAC and North America. Revenue growth of 30% in EMEA probably indicates Adyen is not gaining share as fast as previously. EMEA remains the largest market and accounts for 57% of total net revenues.

EBITDA was up 31% year-on-year to €356m but actually declined slightly from H2 21 to H1 22. Overall margins remain a very healthy 59%. Profits were hit by higher payroll costs as 395 staff were added, together with a sharp increase in travel as employees got back on the road to meet customers and each other. Adyen made a very clear commitment to F2F business life: “It’s clear that building trusted relationships and driving innovation moves faster when time is spent together. The speed and excitement that meeting each other in person brings has always been a crucial part of our success and our view on how to build the Adyen culture for the long term.”

Capex was €40m (up 160bps to 6.6% of net revenue) as a result of the geopolitical crises. “We invested in our data center infrastructure at a larger scale than we would have under different macroeconomic circumstances.”